Homeownership is an aspiration for many, and 65 percent of people in the US already own their homes. But with rising house prices and high demand–primarily in major US cities–renting is becoming a necessity for the younger generations.

Therefore, it would be wrong to dismiss renting outright, even if owning your home has its clear advantages. In order to help you get an idea of the big differences between renting and buying, we’ve put this handy graphic together, along with how policies like homeowners life insurance protect you if you own your own home.

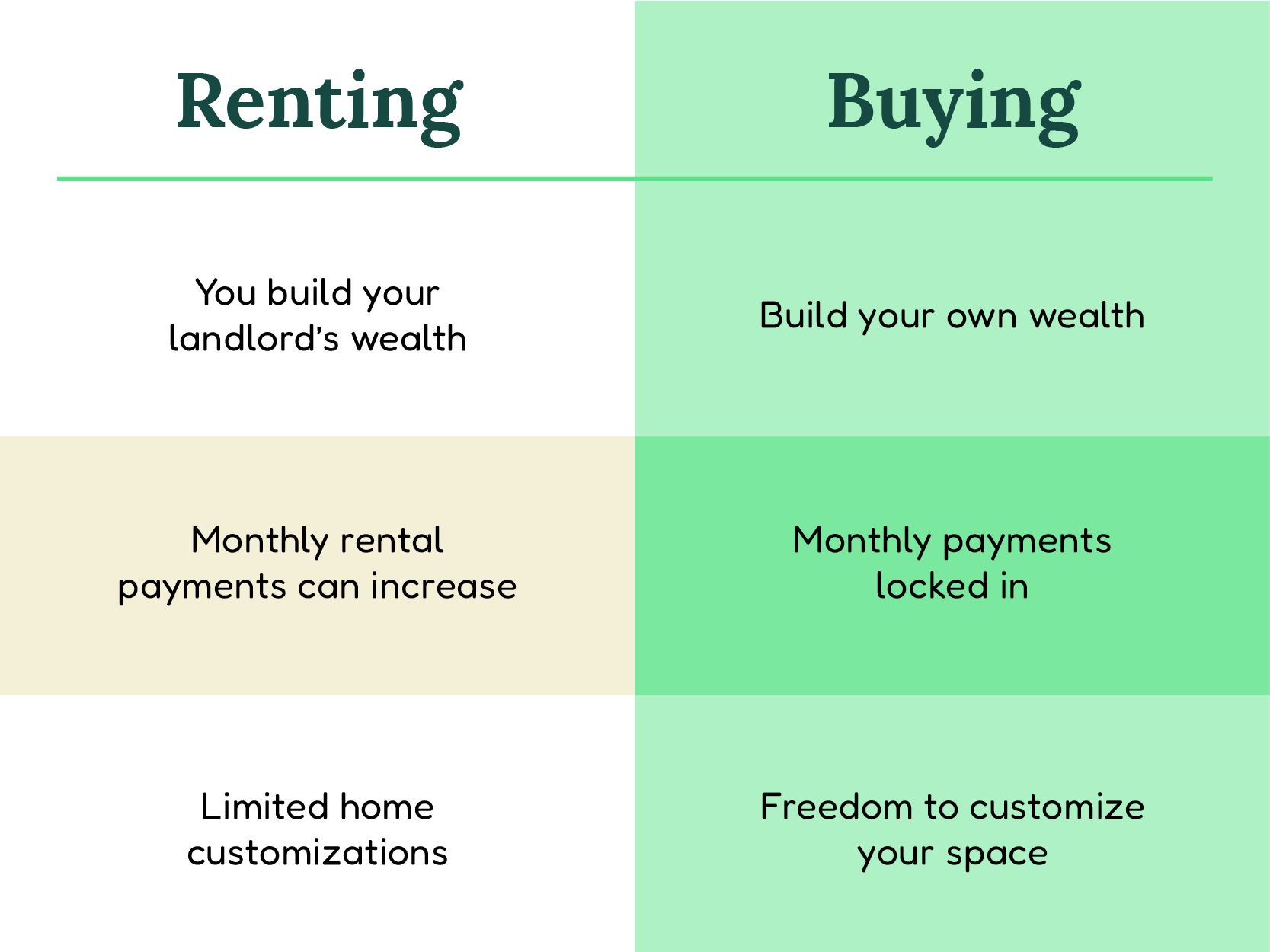

Differences between renting and buying in a nutshell

The key homeownership and renting stats:

- 65% of Americans: the number of US citizens who own their home

- 82.8 million: the number of owner-occupied homes

- 42 million: the number of rented units in the United States

- 93%: Number of Americans who believe owning a home is a better investment than stocks

Advantages of renting

Renting may cost less money

There are fewer financial burdens on renters when they first move in, as the initial investment to rent a home is usually lower than buying. Funds used towards a down payment or higher mortgage repayments can be invested elsewhere.

Fewer responsibilities

There’s no need to take care of repairs when you’re renting. The landlord is responsible for these tasks, meaning you have fewer responsibilities and don’t need to fork out on expensive maintenance costs.

Diversify asset investment

Renting your place means you can diversify your investment opportunities on a broader array of assets, as you aren’t plowing the majority of your resources into where you live.

Advantages of buying

Investment

Buying a home is generally viewed as a solid investment and one of the safest ways to invest your money in the long term. Just this year, house prices have increased by an average of 12%.

Equity

You can enjoy access to equity if your house rises in value over time. Therefore, you could potentially remortgage and borrow more money for other investments or sell at a profit and benefit from increased personal wealth.

More control

As a homeowner you have more control over your home and can decorate as you wish without worrying about what a landlord may think. You also don’t have restrictions on how much noise you make, whether you own pets, and even if you have any children.

Tax breaks

The mortgage interest and some closing costs can be tax-deductible, and you get most of the relief in the early years of homeownership when you’re mostly paying back the mortgage interest.

Lay down roots

If you want to stay somewhere long-term and start a family, buying is a better option than renting. You have your own home and can create long-lasting memories as you raise a family.

Protection

More options available to help safeguard your property against potential issues if you own your home. These include having certain insurance policies on the property, such as homeowners life insurance, to protect your mortgage payments should the worst happen.

How does life insurance protect a mortgage?

Buying a home is typically the largest purchase of your lifetime. And unless you have a Scrooge McDuck money pit lying around, there’s every chance that you will need to purchase your house with a mortgage.

That means having the single-largest debt you’re ever likely to owe. There are risk elements whenever you go into debt, even if it’s for something like a mortgage, which is regarded as a relatively safe bet.

Therefore, it’s only natural that you would want to protect yourself should you become unable to keep up with payments. Having homeowners life insurance can do just that and help you and your family keep up with mortgage payments should you become sick or even worse.

Should I buy or rent my homeowners life insurance policy?

One can opt to get a term policy that covers the length of the mortgage. This is because they just want the coverage while the mortgage is still outstanding. If the worst happens, they’re happy knowing that their loved ones will be left with a death benefit that covers the mortgage.

Average length of mortgage: 30 years (it’s a big commitment)

A life insurance policy can be matched to the mortgage length

However, this isn’t always the best option, as you’re effectively renting your life insurance without any return unless you were to pass away–and no one wants that. Once the policy has finished, you will have made all the payments but don’t get anything back.

Therefore, it could make sense to own your policy with permanent life insurance. A permanent life insurance policy gives you a death benefit like a term policy–your loved ones will still receive a payout that can cover the mortgage payments if you die. But it also acts as an investment vehicle that you can use while you're still alive and, unlike term, the coverage period is your entire life rather than expiring after 20 or 30 years.

That's because it has a cash-value element that increases over time. Essentially, it grows on top of your original coverage amount and can be accessed tax-free later in life. So if you make all your mortgage payments without any issues, you can use your permanent life insurance policy for retirement, a down payment for an investment property, or whatever you wish.

Learn more about a permanent life insurance policy.

Isn’t permanent life insurance expensive?

Yes, permanent life insurance is more expensive than term. Typically what we suggest for someone who’s interested in having their full mortgage covered while still reaping the long term benefits (such as tax-free cash and ongoing protection) of permanent life insurance is to get a combination policy. This allows you to access a higher coverage amount for 20 or 30 years, after which your coverage amount reduces. However, that’s when you’ve paid off your mortgage and won’t need as much coverage, but you’ll still be able to access tax-free savings and have some amount of permanent protection, all for a reasonable price.

In conclusion: protecting your property

There are some big differences between renting and buying, chiefly that buying gives you an asset you own that can grow in value over the long term. And if you want to protect that asset, getting permanent homeowners life insurance can reduce the risk around mortgage payments while helping to look after your future.

Checkout options for a homeowners life insurance policy today.