There are two things guaranteed in life: death and taxes. But did you know there is a way to use your death benefits to reduce your taxable income when you’re retired?

When you retire, you get to leave behind your alarm clock, the commute, and cranky coworkers. But what will never leave you is that tax bill for your income — in fact, for many retirees, income tax is their largest single expense.

You might be thinking, “Income taxes? How am I being taxed for income when I have no job?”

While you’ve given up the rat race, you are still garnering an income through social security benefits, a pension, or a tax-deferred investment such as a 401(k), 403(b), or an IRA. Your tax rate will depend on the amount of retirement money you are withdrawing throughout the year (or the lump sum, if you’ve chosen one payment annually). So, if your total retirement income for the year is $70,000, you’ll be taxed at the 22% tax rate for single (and married, filing separately) taxpayers.

But there’s a way to get around paying so much in taxes, especially if you are on a fixed income. If you have a permanent life insurance policy, you can use your death benefits or the cash value that you accrue during the life of the policy to supplement your income. That money is not taxable!

How does cash value work?

When you purchase a permanent life insurance policy, many of these policies come with a cash value component, which is a savings account that draws its funds from your monthly premium. So, if your monthly premium payment is $100, $65 could be set aside for the cash value savings. The longer you have your policy, the larger your cash value will be. You can choose to withdraw the fund or take out a low-interest rate loan. Unlike the withdrawal or loan from your 401(k), permanent life withdrawals and loans don't come with any tax penalty. Your cash value builds on top of your death benefit, which you can choose to be a fixed amount for your whole life or decrease as you get older if you want to save on the cost of insurance. If you die before using your cash value, it will pass on tax-free to your beneficiaries along with your death benefit.

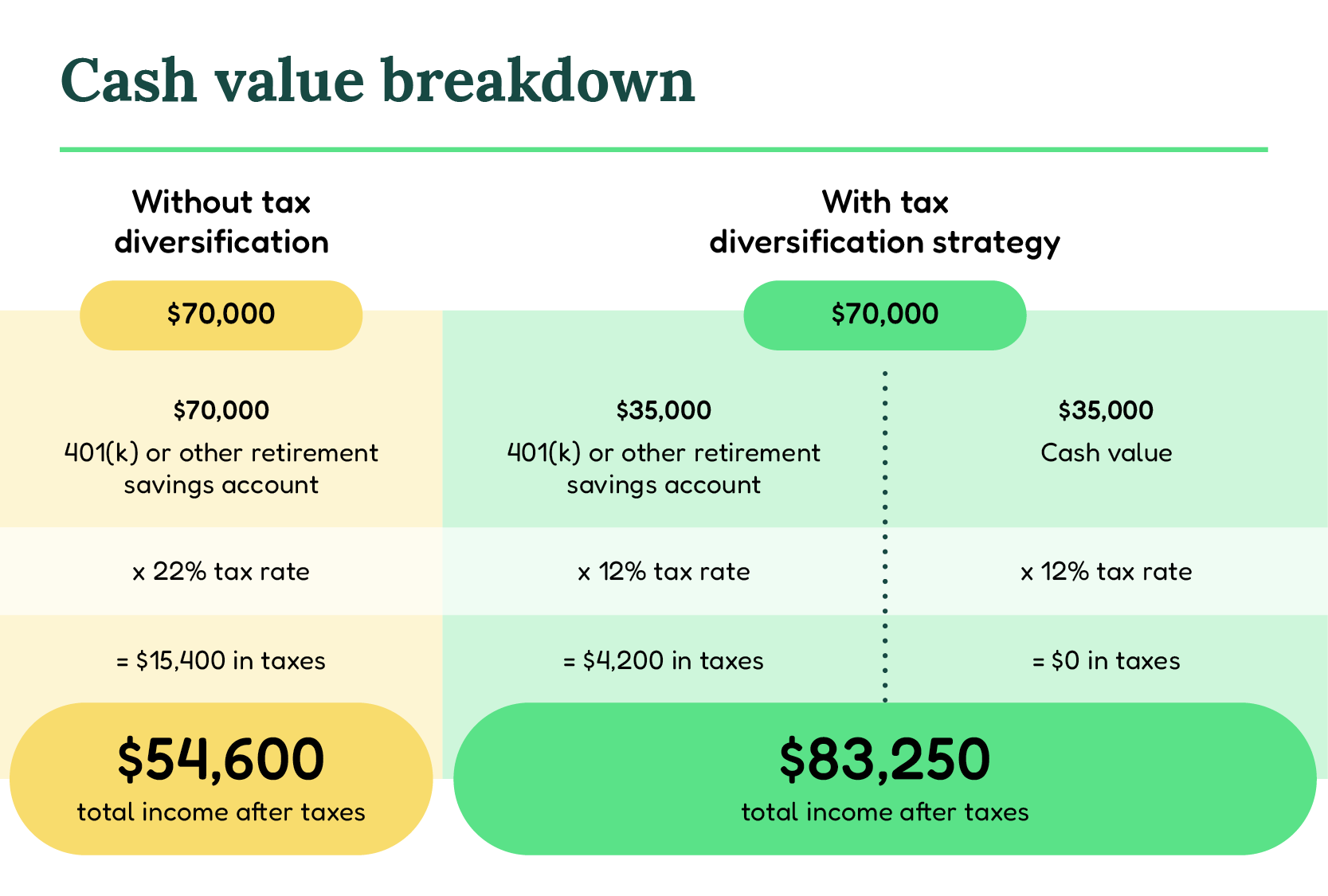

How can you use your insurance policy to reduce your taxable income? A simple but effective way to reduce your taxable income is to rethink your retirement withdrawals. Instead of taking out $70,000 from your retirement savings account each year, you can reduce that amount by half, and take the remaining $35,000 from your permanent life insurance policy. This way you will only be taxed for the $35,000, which is taxed at a lower rate (12%). With this strategy, you have the same withdrawal amount but you increase your post-tax income.

Here’s a breakdown:

Through the tax diversification strategy, you have an additional $11,000 to spend each year that could go towards that Alaska trip you’ve had on your bucket list or to a grandchild’s education fund! There you have it, how to retire smarter — and wealthier — by diversifying into a permanent life insurance policy.