We started Amplify to break down education and access barriers to life insurance and help consumers make one of the important financial decisions in their lives - pick the right products and understand what you are putting your hard earned money into. There are two main types of life insurance:

Term

Created in 1759, it is the oldest and the only form of life insurance before the emergence of permanent life insurance in 1940. Term insurance is a “pure insurance policy” that provides coverage for a set period of time. If you pass prematurely within the policy period, your beneficiaries receive the payout; otherwise, the policy expires and has no other value. Term life insurance in general is simpler and cheaper than permanent life insurance.

Permanent

As the name indicates, permanent life insurance provides lifelong coverage and includes a long term savings vehicle. Since the policy does not expire until end of life, there is a specified death benefit for your beneficiaries. Permanent life insurance has a lot more features - accumulating tax free cash value, borrowing against the policy, etc. - but it is generally more expensive than term insurance. Given the complexity of permanent life insurance, it is very important for you to understand the details before purchasing a permanent policy. There are three main types of permanent life insurance -

- Whole Life (created in 1940)

- Variable Universal Life (created in 1986)

- Index Universal Life (created in 1997)

Comparison

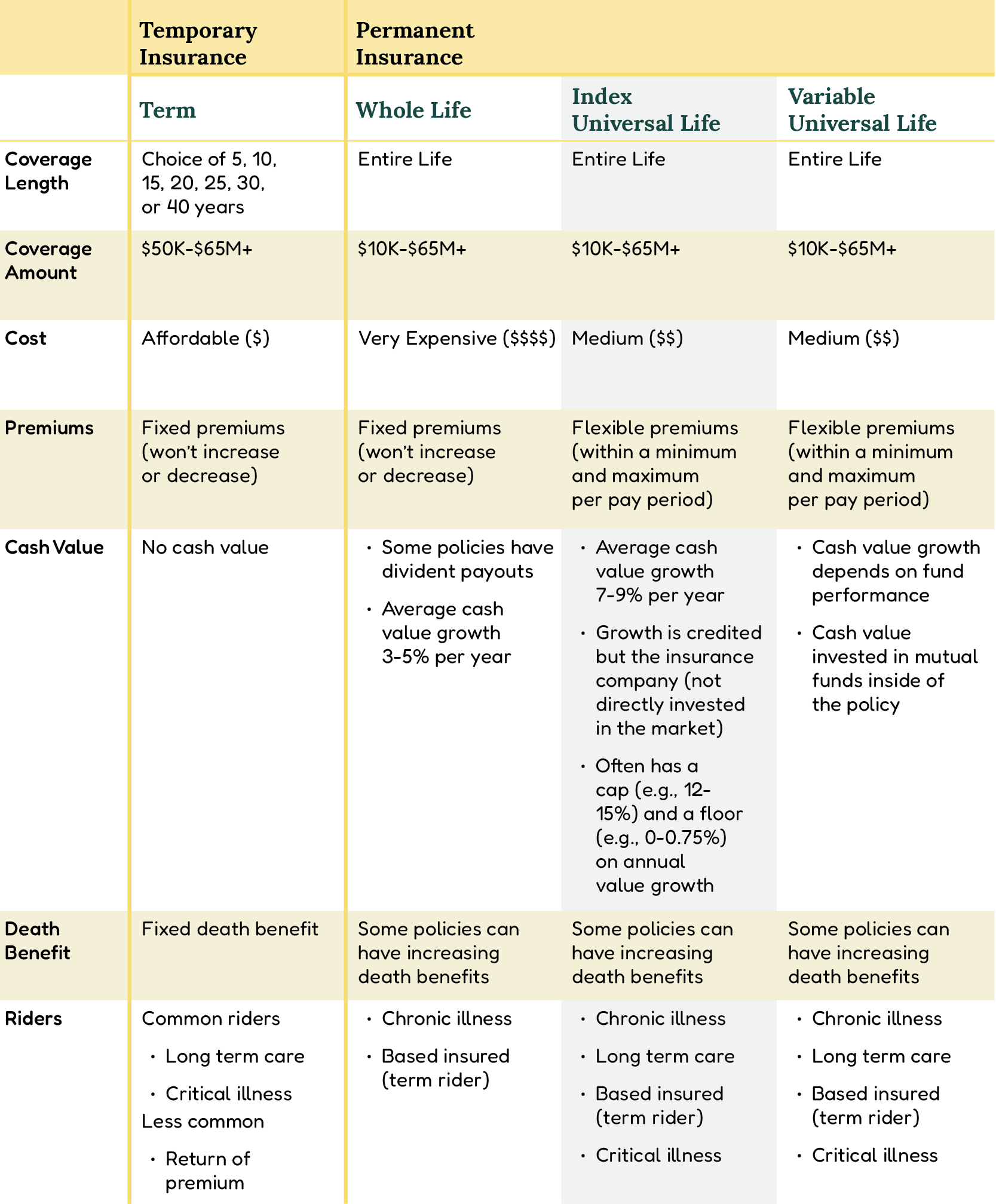

The following table summarizes the differences between term and the main types of permanent life insurance:

Suitability

Term

It is suitable for individuals who - Only need insurance to replace income for a certain period of time, such as raising kids and paying off mortgage Want the most affordable insurance

Permanent

There are several reasons why individuals want the additional offerings provided by permanent life -

- Diversifying their portfolio with a tax advantaged high interest savings vehicle

- Leaving beneficiaries funds that are income tax-free

The different types of permanent life products are designed for individuals with varying degree of risk tolerance. Whole life is designed for the conservative who -

- Prefers a guaranteed return

- Prefers guarantee on permanent life insurance coverage

Index Universal Life is designed for the moderate who -

- Prefers safety but still desires high return

- Is heavily invested in tax-deferred assets (traditional 401K and IRA, etc.)

Variable Universal Life is designed for individuals with higher risk tolerance who -

- Prefers high returns and is comfortable with market risk

- Is heavily invested in tax-deferred assets (traditional 401K and IRA, etc.)