What happens as you age if you require long-term care?

Well, you need to be able to afford your care, for one thing. But planning for retirement, senior insurance, and your older age can be overwhelming. However, long-term care statistics show that planning early is one of the most effective ways to protect your family’s future.

The modern data collected below suggests that long-term care will need to be a consideration for most people, and tax-advantaged permanent life insurance can play a role in covering costs (when structured correctly).

Whether you consider using empty-nest life insurance or another form to establish coverage, these statistics highlight the long-term implications of getting older (and how life insurance can support your needs).

Statistics on long-term care costs

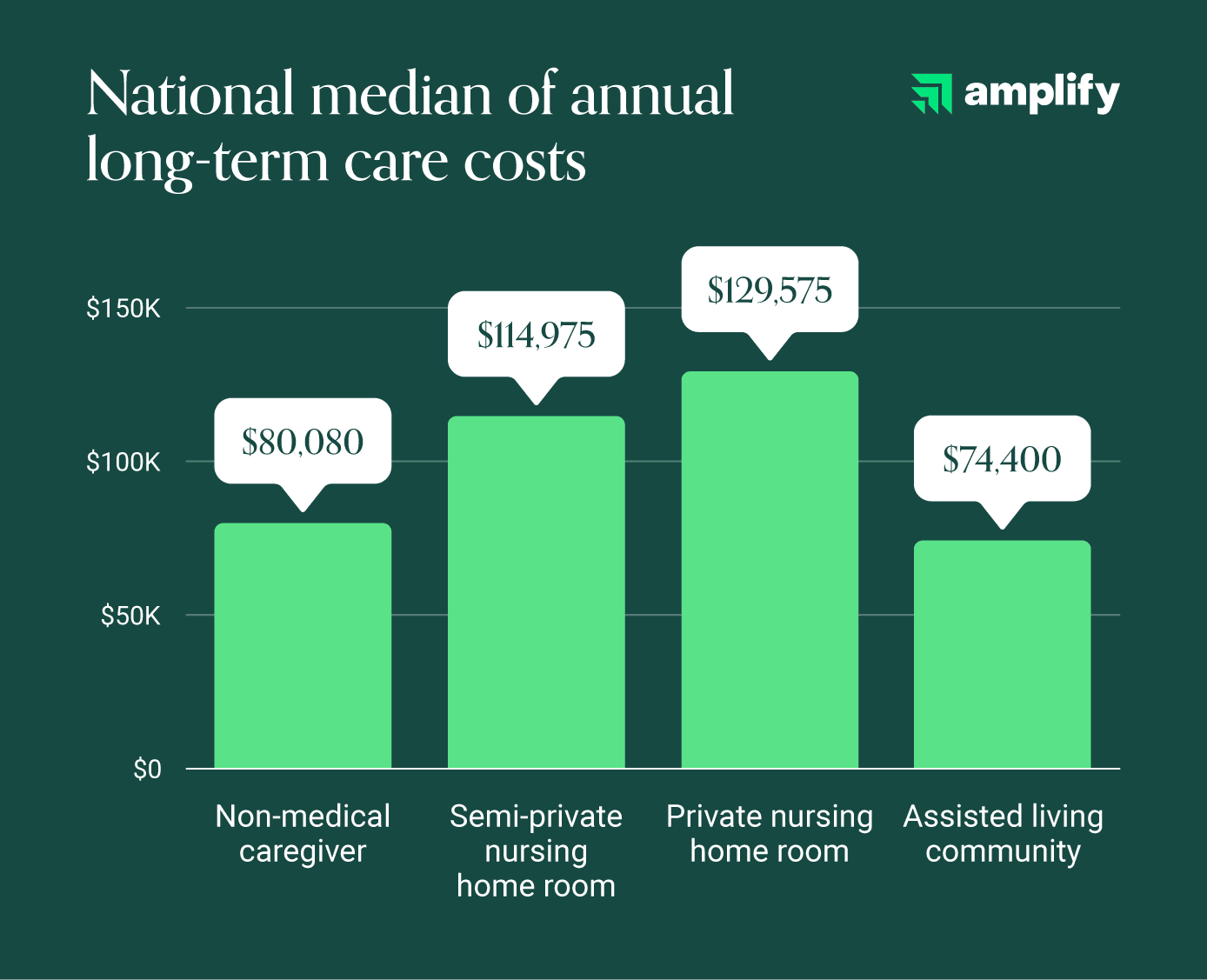

The financial impact of aging is often higher than expected, especially given rising nursing home and assisted living costs. Here are the key facts to know about long-term care costs:

- The national median rate for a non-medical, in-home caregiver is $35/hr. (CareScout)*

- The national median average for in-home skilled nursing services is $90/hour. (Genworth)

- The median per-visit rate for in-home skilled nursing services is $160. (Genworth)

- The annual cost of in-home care is approximately $80,080. (CareScout)*

- The national median cost for a private nursing home room is $129,575. (CareScout)**

- A semi-private room in a nursing home costs an average of $315/day. (CareScout)**

- The cost of assisted living communities increased 5% in 2025. (CareScout)

- Long-term services and support (LTSS) costs increased by almost 50% between 2019 and 2024. (AARP)

Statistics on long-term care costs by state

The national average doesn't pay the bills when nursing home costs in your state are higher than the rest of the country. While the U.S. median is a helpful starting point, care costs are hyper-local. We’ve broken down the data by state to help you see the real numbers, ensuring you specify enough for the place you call home.