Key Takeaways

The best IUL offerings include Amplify, Fidelity & Guaranty, and Pacific Life, which offer a combination of features like easy onboarding, broad index choices, and diverse living benefits.

IULs combine a death benefit and wealth accumulation to be used during your lifetime.

You should choose a plan that aligns with your goals, risk tolerance, and budget.

Building a secure financial future shouldn’t have to be a choice between high-stakes market risk and stagnant savings.

Selecting the best indexed universal life insurance (IUL) is one of the few ways to secure a death benefit for your loved ones while building a tax-advantaged cash reserve that participates in market gains—all without the fear of losing your principal during a market crash.

However, the world of IUL is famously complex, often leaving applicants stuck between choosing a massive, 150-year-old insurance carrier or a modern, tech-driven platform.

Continue reading to gain a deeper understanding of your options and determine which provider is best suited for you.

The best indexed universal life insurance options and providers

Choosing the right life insurance depends on a balance of financial security and modern accessibility. We based our selections on four key pillars:

- Financial strength: We prioritized carriers with “Superior” or “Excellent” ratings from independent rating agencies such as AM Best and S&P Global to ensure they have the long-term capital to pay future claims.

- Digital innovation: For modern agencies like Amplify, we evaluated the ease of the online application process, AI-driven policy customization, and the quality of real-time wealth-tracking dashboards.

- Customer reviews: We analyzed the NAIC Complaint Index and third-party consumer reviews (such as Trustpilot) to measure real-world reliability and customer service responsiveness.

- Product flexibility: We looked for “living benefits,” like long-term care (LTC) riders, diverse index crediting options, and the ability for policyholders to adjust premiums as their financial goals evolve.

Before diving into our top picks, it’s important to distinguish between the two types of companies in this list. While they’re often grouped as “providers,” they play very different roles in your insurance journey:

- Carriers: These are established financial institutions, such as Nationwide or Pacific Life. They design the policies, set the rates, and, most importantly, are the ones who hold your money and pay out the death benefit.

- Agencies: These are companies like Amplify or Ethos. They do not issue the policies themselves. Instead, they act as a modern digital storefront. They use technology to help you compare, customize, and apply for policies from various carriers in one place.

Here’s an overview of the best indexed universal life insurance options:

Provider | Type | Best for | Key features | Coverage | Pricing |

|---|

1. Amplify | Agency/Distributor* | Best overall | AI-driven customization, 100% digital experience, and real-time wealth tracking tools | $50k – $5M+ | Highly competitive; optimized for cash value |

2. Fidelity & Guaranty Life | Carrier | Income stability | Broad index choices (Barclays/Bloomberg) and strong fixed-loan rate options for income | $100k – $5M+ | Moderate; good value for retirement |

3. Transamerica | Carrier | Foreign nationals | Specialized foreign national program and 100% instant decision options | $25k – $10M+ | Very competitive for healthy profiles |

4. Lincoln Financial | Carrier | Estate planning | Strong survivorship (two-life) options and WealthPreserve “no-lapse” guarantees | $100k – $10M+ | Competitive for long-term legacy |

5. Nationwide | Carrier | Long-term care | Top-tier LTC riders and indemnity-style chronic illness coverage | $100k – $5M+ | Average; high value for LTC focus |

6. Mutual of Omaha | Carrier | Simplicity | “IUL Express” simplified issue and easy-to-understand crediting for beginners | $25k – $300k | Affordable for smaller death benefits |

7. John Hancock | Carrier | Healthy lifestyles | Vitality Program rewards and premium discounts for exercise and healthy habits | $50k – $10M+ | Variable (discounts based on activity) |

8. Allianz | Carrier | Maximum growth | "Index Lock" feature, high participation rates, and generous 40% bonus multipliers | $100k – $10M+ | Premium (higher fees for higher growth) |

9. National Life Group | Carrier | Living benefits | Market leader in living benefits and strong mutual structure | $50k – $10M+ | Competitive; strong rider value |

10. Pacific Life | Carrier | High net worth | Specialized products for complex wealth and lower costs on $1M+ policies | $500k – $20M+ | Tiered; efficient for large policies |

11. Penn Mutual | Carrier | Early cash value | Guaranteed policy value enhancement in Year 1 and low early surrender charges | $50k – $10M+ | Efficient; strong early-year liquidity |

12. Ethos | Agency/MGU* | Fast approval | No-medical-exam options, instant decision tech, and simplified online application | Up to $2M | Budget-friendly for healthy applicants |

*Amplify and Ethos are insurance agencies that provide access to policies issued by third-party life insurance carriers. All other companies listed are insurance carriers responsible for policy issuance and claim payments.

1. Amplify

Best overall option

Type: Agency/Distributor

Amplify acts as a high-tech, easy-to-use gateway to the life insurance industry’s most robust products. Amplify provides a comprehensive wealth management platform with tools to help you optimize your payments and track policy performance.

Its proprietary technology allows users to customize an IUL policy based on specific financial goals, whether that’s maximizing tax-advantaged retirement income, funding a child’s education, or efficient estate planning.

By partnering with "A-rated" legacy carriers like Nationwide and Ameritas, Amplify ensures that your policy is backed by multibillion-dollar financial stability while you enjoy a modern, user-friendly interface. Policyholders gain access to a real-time dashboard that tracks cash value growth, making life insurance feel less like a “set-and-forget” expense and more like an active part of a diversified financial portfolio.

Features

- Proprietary customization: AI tools that optimize premium payments to maximize cash value accumulation

- Digital onboarding: Fully online application process with instant quote capabilities and rapid approval tracks

- Wealth tracking dashboard: A unique customer portal to monitor the performance of your index-linked cash account

- 0% loan interest options: Access to policies that feature 0% net cost loans, allowing you to borrow against your cash value efficiently

- Living benefits: All policies include accelerated death benefit riders for chronic, critical, and terminal illnesses

Coverage: $50,000 – $5M+

Pricing: Highly competitive

Pros | Cons |

|---|

Fully digital experience, fast process and approval, and designed with financial wellness goals in mind | Digital-only solution may not be for everyone and it's only partner with specific, highly rated insurance carriers |

2. Fidelity & Guaranty Life

Best for: Income stability

Type: Carrier

Fidelity & Guaranty Life, commonly known as F&G, is a big-name carrier that has been a staple of the industry since 1959. Unlike the digital agencies, F&G is the actual “manufacturer” of the insurance products, specializing heavily in the retirement income space.

Financial professionals frequently cite it as great for clients who want to use their IUL as a supplemental retirement vehicle. Their policies, such as the Pathsetter IUL, are engineered with some of the industry’s most competitive “loan” features, allowing policyholders to access their cash value efficiently when it's time to take income.

Features

- Diverse index selection: Access to unique, multi-asset indices designed to perform across various market cycles

- Fixed and variable loan options: Flexible borrowing rules that allow you to continue earning interest on money you’ve borrowed from the policy

- Overloan protection: A built-in safeguard that prevents the policy from lapsing if you take significant withdrawals in retirement

- Wellness and living benefits: Includes riders for critical and chronic illness at no additional upfront cost

- High premium bonuses: Some products offer "premium credits" or bonuses that give your cash value an immediate boost in the early years

Coverage: $100,000 – $5M+

Pricing: Moderate

Pros | Cons |

|---|

Specialists in retirement benefits, rather than just death benefits, offers some of the lowest net cost loans in the industry, and backed by huge asset reserves | A more formal application process, potentially long wait times for approval, high complexity, usually must work with an agent, and requires paperwork, missing many digital features |

3. Transamerica

Best for: Foreign nationals

Type: Carrier

Transamerica is a global insurance giant that provides coverage for non-traditional applicants, including foreign nationals and residents with unique health profiles. Their Financial Foundation IUL II offers a broad range of index options and is known for its express underwriting track, which provides 100% instant decisions for qualified applicants.

This makes them one of the few legacy carriers to compete directly with digital-first agencies on speed. Additionally, they have some underwriting flexibility, including for applicants with certain health issues or up to higher age limits. This may make Transamerica a reasonable choice if other carriers are less willing to insure you.

Features

- Trendsetter LB: A term-to-permanent option that includes robust living benefits

- Instant decision: The "FFIUL II Express" provides immediate coverage decisions online

- Global reach: One of the best options for individuals living in the U.S. on a visa or with international interests

- Options for a wide range of earners: Their two main IUL policies (Transamerica Financial Foundation IUL® II and Transamerica Financial Choice IUL℠ II) cover a wide variety of people and high earners, respectively

Coverage: $25k – $10M+

Pricing: Very competitive for healthy profiles

Pros | Cons |

|---|

Fast digital underwriting for a legacy carrier, excellent for non-US citizens, and high financial ratings | Customer service wait times can be longer, the web interface is less intuitive than digital-only agencies, and the foreign nationals program is generally geared toward higher‑net‑worth clients |

4. Lincoln Financial

Best for: Estate planning

Type: Carrier

Lincoln Financial is a common choice for families and business owners focused on long-term wealth preservation. Their WealthPreserve IUL products are specifically built for durability, featuring some of the longest no-lapse guarantees in the industry, including some that protect the policy up to age 121.

This makes Lincoln a top choice for estate planning, where the primary goal is ensuring a tax-advantaged death benefit is available to pay estate taxes or fund a trust, regardless of market performance.

Features

- Survivorship expertise: Industry-leading options for insuring two lives under a single, cost-effective contract

- LincXpress® Tele-App: A streamlined application process that allows for “lab-free” approval for qualified applicants up to age 60

- Multiple indexed accounts: Choose from six different index accounts, including the Fidelity AIM® Dividend Index for smoother, low-volatility growth

- Chronic illness riders: Offers robust living benefits that allow you to access the death benefit early if you require long-term care

Coverage: $100,000 – $10M+

Pricing: Competitive (for guarantees)

Pros | Cons |

|---|

Ideal for legacy building with guaranteed payouts, efficient application process with their tele-app, and strong asset protections for business owners | Slightly lower growth caps than other carriers, complex riders that often require professional guidance, and limited initial liquidity |

5. Nationwide

Best for: Long-term care

Type: Carrier

Nationwide is considered a good choice for living benefits, thanks to its industry-leading LTC rider. While many IULs offer basic illness riders, Nationwide’s LTC Rider II provides an indemnity-style benefit.

This can be a big advantage. Unlike other reimbursement-style plans that require you to submit receipts, Nationwide simply sends you a monthly check once you qualify for care. This gives you total flexibility to pay family caregivers or modify your home.

Features

- Automatic chronic/terminal riders: Includes standard living benefits on almost every policy at no extra charge

- Overloan lapse protection: A built-in feature that prevents the policy from lapsing if you have a large outstanding loan in your later years

- Nationwide intelligent underwriting: A streamlined process that can offer lab-free approvals for healthy applicants

Coverage: $100,000 – $5M+

Pricing: Average

Pros | Cons |

|---|

Excellent LTC protections, consistently score high in customer satisfaction, and a flexible reimbursement model | Less growth-focused with lower caps, LTC Rider II comes with an additional cost that increases the premium, and the LTC claims process can be complex |

6. Mutual of Omaha

Best for: Simplicity

Type: Carrier

Mutual of Omaha is known for reliability and straightforward products. Their IUL Express® product is specifically designed for those who want the benefits of an indexed policy, such as downside protection and cash accumulation, without the complexity often found in high-end wealth products.

It’s one of the few simplified issue IULs on the market, meaning it’s designed for a faster, easier application process that avoids the heavy medical requirements of traditional permanent life insurance.

Features

- Guaranteed no-lapse: Includes a protection period (often up to 20 years or age 80) that ensures the policy stays active as long as minimum premiums are met

- Three-in-one living benefits: Built-in riders for chronic, critical, and terminal illness included at no additional upfront cost

- Flexible premium payments: Allows you to adjust your contributions as your household budget changes

- Proton® index options: Access to volatility-controlled index options for more consistent, smooth growth

Coverage: $25,000 – $1M+

Pricing: Affordable

Pros | Cons |

|---|

User-friendly interface, some of the lowest entry-level coverage amounts in the IUL space, and high focus on policyholder stability and long-term financial strength | Possibility of lower growth potential, the express track is typically only available up to $300,000, and traditional interface, lacking real-time wealth tracking |

7. John Hancock

Best for: Healthy lifestyles

Type: Carrier

John Hancock stands out in the IUL market through its unique vitality program. Unlike traditional policies that only pay out at the end of life, John Hancock’s IUL is designed to be an active part of your daily routine.

By participating in the vitality program, policyholders can earn “status” by completing simple health-related tasks, such as walking, getting a flu shot, or buying healthy groceries. These points translate directly into premium savings (up to 25%) and external rewards, such as discounts on wearable fitness devices, travel, and even retail gift cards.

Features

- Galleri multi-cancer screening: Eligible members with $500k+ in coverage can access advanced early cancer detection tests, often fully subsidized

- High issue age: One of the few carriers to offer coverage to applicants as old as age 90

- Quit smoking incentive: Allows smokers to pay non-smoker rates for the first three years if they commit to quitting

- Flexible crediting: Offers diverse index options, including the S&P 500 and specialized global indices

Coverage: $50,000 – $65M

Pricing: Variable (discount driven)

Pros | Cons |

|---|

Can earn additional benefits and money back with healthy lifestyle choices, capable of handling very large face amounts (up to $65M) for complex estate needs, and consistently earns A+ (Superior) ratings for financial strength | Requires tracking activities to receive favorable rates, must work through an agent to get a quote, processing can take weeks or longer, and not a good option for people who are less active or healthy |

8. Allianz

Best for: High potential growth

Type: Carrier

Allianz Life is a global heavyweight and a primary carrier of IUL products. They’re widely regarded as the inventors of the index lock feature, which allows policyholders to lock in their gains at any point during the year if they believe the market has peaked.

This makes Allianz a choice for more active policyholders who want a hand in managing their cash value month-to-month. Their Life Pro+ Advantage product is specifically designed for high accumulation potential and features some of the highest participation rates in the industry.

While their products are feature-rich, they’re also complex, often requiring the guidance of a professional to navigate the various crediting methods and bonus structures.

Features

- Index lock feature: Provides the unique ability to lock in index interest at any point during the crediting period

- Multiple bonus options: Offers multiple versions of their plans to let users trade higher fees for higher growth potential

- Global stability: Holds an A.M. Best “A+” (Superior) rating, representing the highest tier of financial strength

- Diverse allocation: Access to exclusive indices that aren't available through smaller boutique carriers

Coverage: $100,000 – $10M+

Pricing: Premium

Pros | Cons |

|---|

High participation rates, high degree of control with index lock, and massive cash reserves | Complexity can be overwhelming for first-time buyers, higher fee structures, and the application process can be paperwork-intensive |

9. National Life Group

Best for: Living benefits

Type: Carrier

National Life Group (NLG) is a pioneer in the living benefits space, offering a comprehensive suite of riders that allow policyholders to access their death benefit early for chronic, critical, or terminal illnesses. As a mutual company, NLG is owned by its policyholders, which often leads to a long-term focus on policy value rather than quarterly stock performance.

Their FlexLife IUL is one of the most popular products in the industry, specifically designed to bridge the gap between death benefit protection and cash accumulation for the middle market.

Features

- Accelerated benefits: Industry-leading riders included at no additional cost for most policies

- Mutual structure: Policyholder-owned, providing strong alignment with long-term consumer interests

- High performance ranking: Frequently ranked as a top provider for total indexed life sales

Coverage: $50k – $10M+

Pricing: Competitive; strong rider value

Pros | Cons |

|---|

Strong living benefits, mutual company stability, and simplified issue options for up to $3M | The application process is agent-heavy and policy loans may impact dividend earnings |

10. Pacific Life

Best for: High net worth individuals

Type: Carrier

Pacific Life is considered a legacy carrier and is a favorite for affluent individuals and business owners. They offer a sophisticated suite of IUL products, such as Pacific Horizon ECV, which is specifically designed for early cash value (ECV).

This is critical for businesses that want the benefit of life insurance without a major investment in the first few years. Their products are built for high-limit strategies, often used for executive bonus plans, split-dollar arrangements, and complex estate tax funding.

Features

- Customized survivorship options: Excellent second-to-die policies for efficient wealth transfer to the next generation

- Smooth performance accounts: Access to accounts like the BlackRock iShares® or Pacific Life Floating Mid-Cap for diversified growth

- High-capacity underwriting: Equipped to handle massive face amounts and complex corporate-owned life insurance (COLI)

- 0% net cost loans: Offers standard loans that eventually become 0% net cost, allowing for tax-advantaged income

Coverage: $500,000 – $20M+

Pricing: Tiered

Pros | Cons |

|---|

The application process is agent-heavy and policy loans may impact dividend earnings | Not ideal for entry-level buyers, high premiums, must work through an agent, no online options, and very thorough medical and financial vetting process |

11. Penn Mutual

Best for: Early cash value

Type: Carrier

Penn Mutual is known for being incredibly agent-friendly and efficient. As a mutual company (owned by policyholders), they have a long history of financial strength and conservative management.

Their IUL products, like accumulation VUL/IUL, are highly regarded for their early surrender value riders. While most IULs take 10 to 15 years for the cash value to equal the premiums paid, Penn Mutual allows for much faster liquidity, which is a major draw for people who want access to their cash value in the early years.

Features

- ACE underwriting: Accelerated client experience is a high-limit, lab-free approval process that is significantly faster than traditional carrier routes

- Guaranteed multipliers: Many of their plans include policy value enhancements that act as a guaranteed bonus starting in year one

- Direct recognition loans: Offers a transparent loan system that is ideal for those who plan on borrowing against their policy frequently

- Superior financial ratings: Maintains an A+ (Superior) rating and a very low complaint index

Coverage: $50,000 – $10M+

Pricing: Efficient

Pros | Cons |

|---|

Access to early cash value, a combination of speed and reliability, and reputation for transparency and realistic growth projections | Focused primarily on financial growth, missing some final expense features, fewer boutique or international index options, and lower growth projections |

12. Ethos

Best for: Fast approval

Type: Agency/MGU*

Ethos is well known for its speed, aiming for “frictionless” fulfillment. Like Amplify, Ethos is a digital agency that uses a high-tech platform to connect users with policies from top-tier carriers, such as Legal & General or Ameritas.

Their standout feature is their proprietary underwriting engine, which can process thousands of data points in seconds to offer instant approval for IUL policies. This makes them a primary choice for healthy applicants seeking a permanent policy without the traditional weeks-long wait for blood tests and medical exams.

Features

- Instant decision technology: Most qualified applicants receive approval in minutes rather than weeks

- No medical exams: For policies up to $2 million, many users can skip the medical exam

- Guaranteed death benefit: Offers options with a 20-year no-lapse guarantee, ensuring protection even in volatile market years

- Convertible options: Provides an easy path for users to start with term insurance and ladder into a permanent IUL later

- Lifetime income rider: Features an optional rider that allows you to convert cash value into a guaranteed monthly stream later in life

Coverage: Up to $2M+

Pricing: Affordable

Pros | Cons |

|---|

Quick quotes and approval, simplified underwriting with no medical exam required (on a case-by-case basis), and users like their simple, easy-to-use interface | Missing the customizations offered by other carriers in favor of simplicity and speed, not ideal for high-net-worth individuals, and offerings are basic |

What is indexed universal life insurance?

Indexed universal life insurance has two parts: The traditional death benefit that goes to your beneficiaries and the cash value element that is meant to be used while you’re alive.

The policy's cash value is tied to an index, such as the S&P 500. However, it’s not actually a direct investment. The provider uses the index to determine your interest rate. This creates the ideal balance of market-linked growth and security, with guardrails in the form of floors and caps.

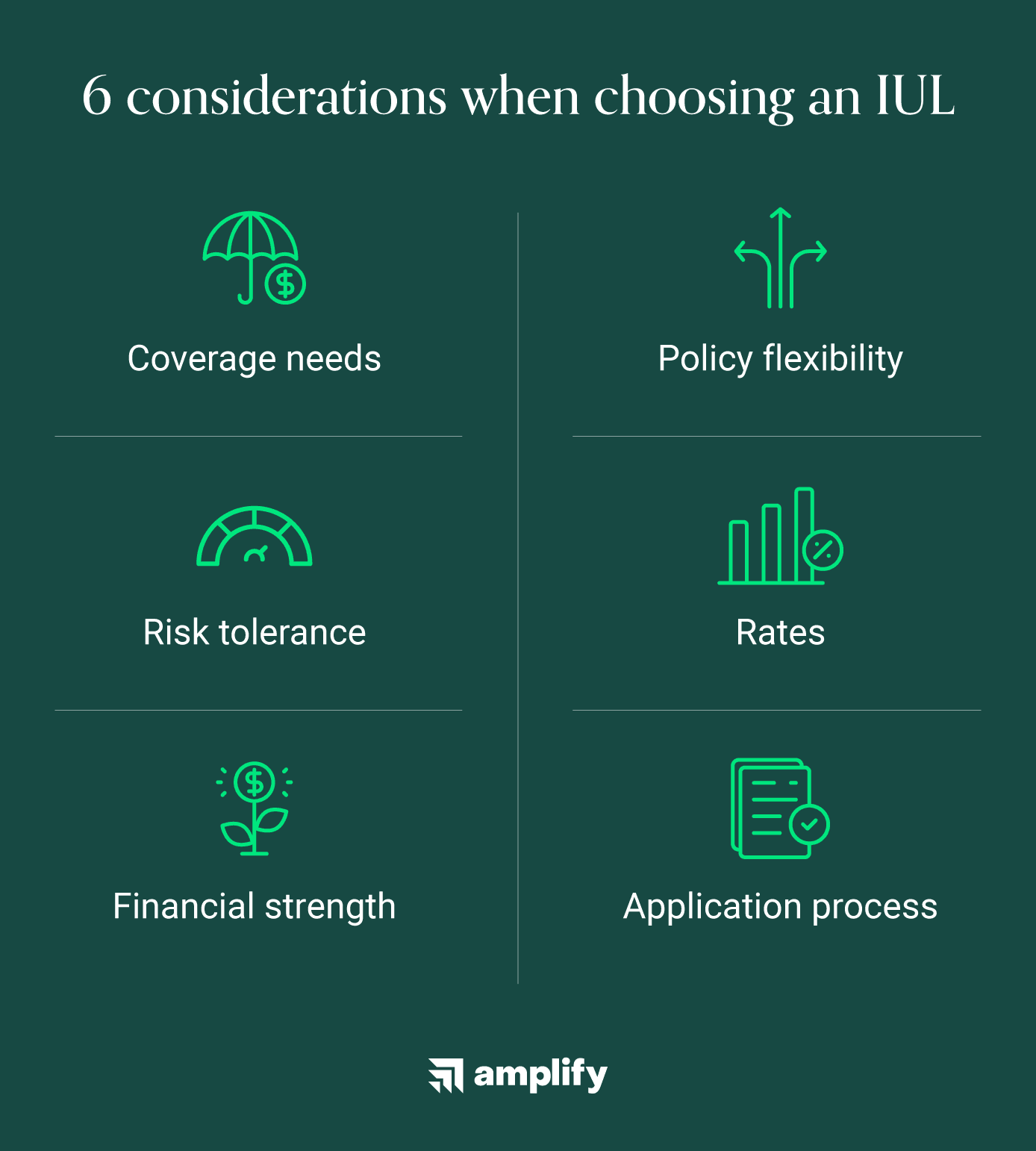

How to choose an IUL company: 6 factors to consider

Choosing the right IUL provider requires a strategic assessment of how a policy fits with your broader financial goals. Since these are permanent products designed to last decades, you shouldn’t just look for a low premium.

You’re also looking for a wealth-building tool that balances immediate accessibility with long-term institutional stability. Whether you prioritize rapid digital growth through an agency or the high-limit guarantees of a legacy carrier, the following six factors should help guide your decision:

- Coverage needs: Determine the primary purpose of your policy, such as replacing income for a growing family or providing a tax-advantaged legacy for your family.

- Risk tolerance: IULs offer a best-of-both-worlds scenario with a 0% floor, but your comfort with volatility will dictate which index options you choose.

- Financial strength: Because an IUL is a long-term contract, the claims-paying ability of the underlying carrier is paramount. Always check independent ratings to ensure the company has the reserves necessary to honor your policy 40 or 50 years from now.

- Policy flexibility: Life circumstances change, and your policy should be able to change with them. Look for flexible premium features that allow you to skip or reduce payments during lean years, as well as the ability to adjust your death benefit without triggering a completely new medical exam.

- Rates: In the IUL world, rates refer to both your monthly premium and the internal cost of insurance (COI) fees. It is vital to compare how much of your dollar is going toward protection versus how much is funneled into your cash-accumulation account.

- Application process: Consider how much time you’re willing to invest in the onboarding phase. Modern digital agencies like Amplify can often provide lab-free approvals in minutes. In contrast, traditional legacy carriers may require a more thorough medical and financial underwriting process that takes several weeks.

Invest in your life with Amplify

Choosing the best indexed universal life insurance requires finding the specific balance of growth, protection, and flexibility that fits your unique financial needs. By understanding the distinction between modern digital agencies and legacy carriers, you can find a policy that provides both the security you need for today and the wealth-building potential you want for tomorrow.

If you’re ready to take the next step toward tax-efficient growth and lifelong protection, you can get a quote with Amplify today.

Frequently Asked Questions

Note

This article is for general educational purposes only and is not intended as financial, tax, or legal advice. Life insurance is not an investment. Indexed universal life insurance involves costs and charges that may impact policy values. Cash value growth is not guaranteed and depends on policy terms, index performance, caps, participation rates, and carrier crediting practices. Loans and withdrawals may reduce policy values and death benefits and may have tax consequences if the policy lapses or becomes a modified endowment contract (MEC). Tax treatment depends on individual circumstances and current tax law, which is subject to change. Product features and availability vary by state and carrier.