This article is provided by Amplify for informational marketing purposes and compares Amplify’s platform with Ethos based on publicly available information and general product descriptions as of 3/13/2026. Product availability, pricing, underwriting requirements, and features vary by state, carrier, and applicant. This overview is not exhaustive and should not be relied on as individualized advice. For the most current details, please review the insurer/carrier policy documents and the competitor’s website.

Amplify vs Ethos: Online Life Insurance Platforms, Compared

Hannah Reifer, Content Marketing, Amplify Life Insurance

Mar 13, 2026

Overview

- Amplify Life vs. Ethos: Comparison chart

- What is Amplify?

- What is Ethos?

- The difference between Amplify and Ethos

- How to choose a life insurance company (and platform) online?

- Amplify your financial future with cash value building policies

Shopping for life insurance online? You've probably seen Amplify and Ethos pop up in your search. Both offer online applications and access to life insurance coverage, but they're designed for different needs.

The difference between Amplify and Ethos comes down to policy specialization, coverage types, and long-term planning considerations. In this article, we'll compare the two platforms and their core service offerings so you can make an informed decision.

Disclosure: Amplify and Ethos are insurance distribution platforms; policies are issued by unaffiliated life insurance companies, and availability, pricing, and features vary by state and underwriting.

Amplify Life vs. Ethos: Comparison chart

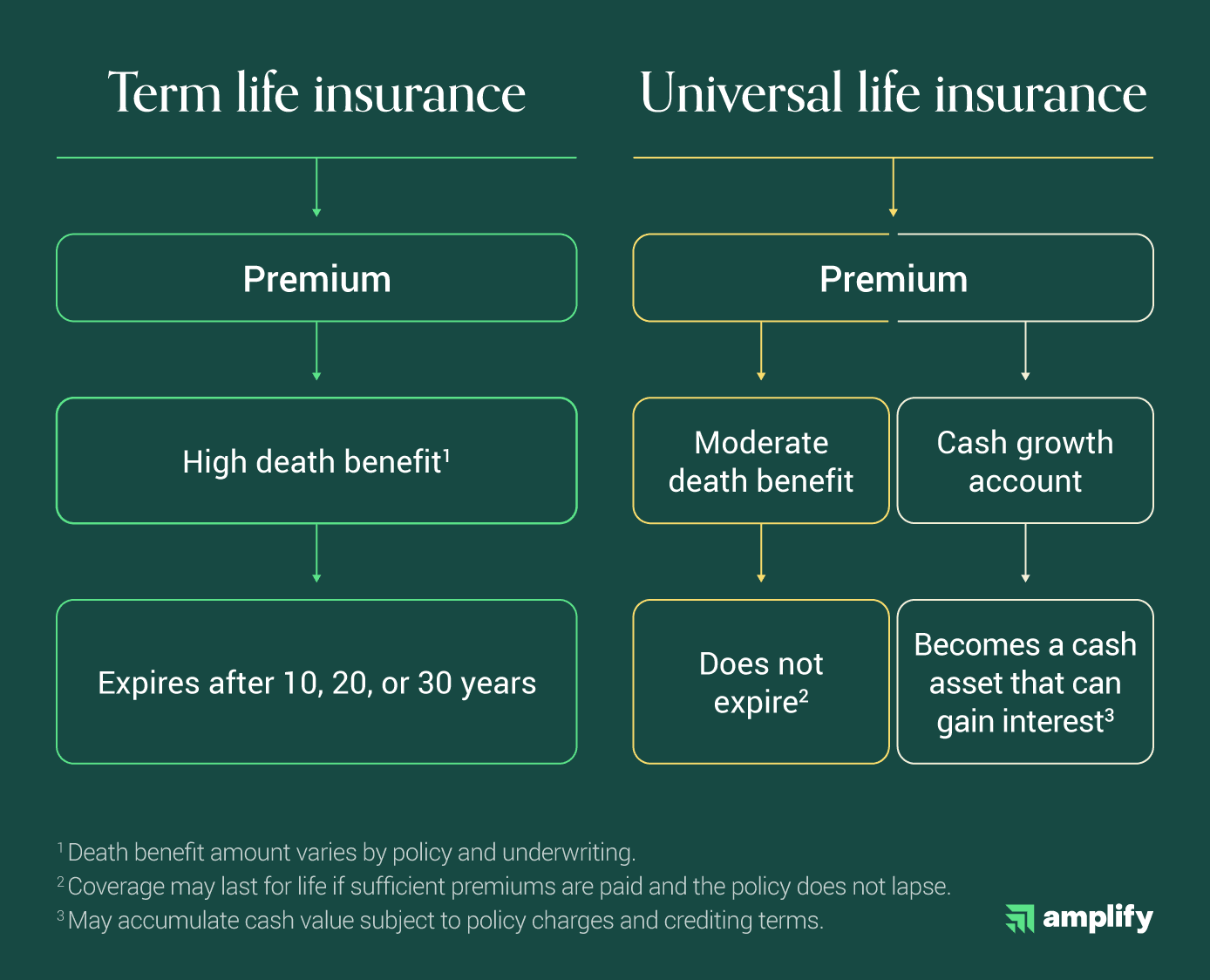

Amplify Life and Ethos play a role in applying for life insurance policies through their digital platforms. They both provide access to multiple kinds of life insurance, but Amplify is more focused on indexed universal life insurance (IUL), and Ethos is more focused on term life insurance.

What does that really mean for you?

- Amplify may be a good fit if you want to explore cash-value life insurance (including IUL/VUL/combination designs) that provides a death benefit and may build cash value, subject to policy terms.

- Ethos may be a good fit if you want straightforward term coverage and prefer to prioritize lower premiums, depending on underwriting.

Amplify Life | Ethos | |

|---|---|---|

May be a fit for | Flexible IUL and VUL options that may build cash value in addition to providing a death benefit; some policies may offer optional riders that can provide benefits during life (availability varies; terms apply) | A variety of term-focused options; coverage amounts (including up to $3 million) may be available for some applicants and vary by age, health, state, and underwriting |

Insurance types | Indexed universal life, variable universal life, combination life, and term life | Term life, whole life, indexed universal life, and final expense insurance |

Application process | Online application; decision timing varies and may require additional information and/or a medical exam, depending on the policy and underwriting | Online application; decision timing varies and may require additional information and/or a medical exam, depending on the policy and underwriting |

Underwriting | Policies are issued and underwritten by unaffiliated life insurance carriers; carrier availability varies by state and product | Policies are issued and underwritten by unaffiliated life insurance carriers; carrier availability varies by state and product |

Policy selection | Focused on IUL and VUL selection, offering a variety of options to fit different budgets | Focused on term life options designed to be straightforward to apply for; eligibility is subject to underwriting |

What is Amplify?

Amplify is a digital life insurance platform/agency that helps you compare and apply for policies online. It simplifies the insurance application process and provides you with professional support along the way.

Amplify’s specialty: Cash-value life insurance options (IUL, VUL, and combination designs)

Specializing in IUL, VUL, and combination policies, Amplify helps families use life insurance to build financial security. These policies offer:

- Protection beyond death benefits: Life insurance doesn't have to be only something that pays out after you pass away.

- Tax-advantaged cash value accumulation: If you're a busy professional looking for more opportunities for tax-advantaged cash value accumulation, these policies can play a role in building long-term wealth. (Tax treatment depends on your situation and policy design; consult a qualified tax professional.)

- Living benefits: Some policies may allow access to cash value through loans or withdrawals (which reduce benefits and may have tax consequences). Some may offer optional accelerated benefit riders for qualifying events (terms apply).

The insurance protects your loved ones, and the policies may also build long-term cash value (depending on funding, costs, and performance).

Amplify also offers term and combination life insurance products, and you can take a quiz to assist with selecting a policy based on your needs and finances. Since Amplify is a team of specialists that offers many different policies, you’ll be able to compare a variety of products and make an informed choice for your family.

Types of life insurance Amplify offers

Amplify offers the following types of life insurance:

- Indexed universal life (IUL): A life insurance policy where a portion of your premiums may go towards cash value, which may grow tax-deferred. Interest credits are based in part on an index-linked formula and are subject to caps/participation rates/spreads and may be 0% for a period. Policy charges and expenses apply and can reduce cash value.

- Variable universal life (VUL): Like an IUL, a VUL allows you to set aside a portion of premiums, although here it’ll go into an actual separate account. They have a higher potential for growth but also a higher risk because the cash value is invested in underlying investment options (often called subaccounts), and can increase or decrease based on performance. VUL involves investment risk, including loss of principal.

- Term life: When most people think about life insurance, they probably picture standard term life policies, which cover you for a certain number of years. Term life is generally simpler than permanent insurance and often has lower initial premiums for the same death benefit. Coverage ends at the end of the term unless renewed or converted (if available) under the policy’s terms; renewal premiums typically increase with age.

- Combination life: This type of policy combines the large death benefit of term life insurance with permanent life insurance that has a cash value portion. Some policies pair a permanent base policy with a term rider for additional temporary coverage; availability and structure vary by carrier and product.

Pros | Cons |

|---|---|

Specializes in IUL and combination policies that may build cash value in addition to a death benefit, with multiple options for your risk and growth preferences | IUL, VUL, and combination policies are often more expensive than term policies, because they’re permanent and offer cash value accumulation |

Simplifies complex IUL, VUL, and combination policies to help you understand options and complete the application | Policies can have variable premiums that you must manage to keep the policy effective and in good standing |

A team of licensed insurance agents ready to help you make sense of the life insurance industry and choose a policy | Policies can have complex terms and conditions |

Digital-first platform that helps you choose policies based on your situation and needs | Policies have varying levels of risk, and cash growth is not guaranteed |

Apply easily online | |

Dedicated case managers assist with the underwriting process | |

Ongoing support before, during, and after you apply for your policy |

What is Ethos?

Ethos is a digital insurance platform similar to Amplify; however, it has a different product focus. Focusing on term and whole life insurance policies, Ethos is a good way to find coverage that’s straightforward and simple, with pricing that varies by underwriting.

Ethos often offers options that may not require a medical exam for eligible applicants, depending on the policy and underwriting. This may shorten the process for some applicants, though it’s important to note that coverage begins only after the policy is issued and the first premium is paid, per policy terms. This makes it ideal for people who want basic insurance structures and low premiums. For example, Ethos offers small final expense insurance plans for modest death benefits. Combined with will and trust planning services, the platform helps make end-of-life planning easier.

Ethos offers the following types of life insurance:

- Term life: One of Ethos’ main product offerings, its term life policies offer numerous term lengths and coverage amounts that vary by state and underwriting; coverage up to $3 million may be available for some applicants.

- Whole life: A kind of permanent insurance policy that may include guaranteed policy values and may pay dividends depending on the carrier (dividends are not guaranteed). Features and performance vary by policy.

- Guaranteed issue life: These policies don’t depend on medical underwriting, and so they’re options for people who are denied for other kinds of insurance. They generally have a graded/limited death benefit period (waiting period).

- Final expense life: Intended only to cover end-of-life costs, these policies are permanent, with small death benefits and stable premiums.

- Indexed universal life: Like Amplify, Ethos offers IUL policies that may play a role in building cash value in addition to providing a death benefit.

Pros | Cons |

|---|---|

Specializes in simple policies with low premiums (depends on underwriting) | Fewer universal life options if you’re looking for policies to help you grow your cash value and get access to that cash while you’re alive |

Specializes in policies with no exam required for eligible candidates | No exam insurance policies may have lower death benefits or higher premiums |

Policy options for people who struggle to get life insurance due to their medical history or age | Term life insurance expires, so while it’s good for temporary protection, it doesn’t build cash value if you outlive it |

Policy options for small end-of-life expenses | Focused on finding the simplest and most inexpensive option, so they may not be the right platform for people who want additional vehicles for their overall financial planning |

Digital-first platform that helps you choose policies based on your situation and needs | |

Apply online with fast approvals, and find out if you qualify to skip a medical exam |

The difference between Amplify and Ethos

Amplify and Ethos are both digital platforms that help consumers shop for life insurance, but they focus on different sets of policy products. While some of their products overlap, the core difference is in which policies each platform specializes.

Ethos focuses on term coverage and simplified permanent options. The platform emphasizes straightforward coverage and may also offer estate planning tools through partners.

Amplify emphasizes cash-value life insurance options that may build cash value and may offer optional riders, depending on the policy. Universal life policies can be more complex; Amplify provides education and application support.

While universal and combination life insurance policies can be more complicated than other types of policies, Amplify makes understanding them simple, and the platform gives you ongoing support with your coverage.

- Amplify may be a fit if you want to explore cash-value life insurance options that may build cash value while providing a death benefit. Pricing varies based on underwriting and product features.

- Ethos may be a fit if you want a streamlined application process and may qualify for a no-exam option, depending on the policy and underwriting.

How to choose a life insurance company (and platform) online?

A good choice is a company and policy that fit your needs, budget, and time horizon. There are many different insurance providers and policy products in the USA, and each platform or broker has a different selection of plans, specialties, support, and features.

Platforms like Amplify and Ethos act as insurance brokers, licensed to discuss options and assist with applications. Part of that job is assisting you with applications and helping you manage your policy.

As of March 2026, both Ethos and Amplify have 4.8 ratings on TrustPilot. Reviewers of Amplify Life often mention a great experience with representatives, noting that they’re helpful, knowledgeable, and positive professionals.

So, when it comes to choosing between Amplify vs. Ethos:

- Amplify may be a fit if you want to explore cash-value life insurance options and want support understanding universal/combination policy features. Amplify is a top-rated life insurance company for robust coverage that works for you while you’re alive. Their representatives specialize in universal and combination life, so they’re well-equipped to help you make sense of the complexities of those policies.

- Ethos may be a fit if you want straightforward term coverage and a streamlined application process; timing and eligibility vary by underwriting. If you're looking for basic term life protection without the complexity of building cash value, Ethos makes it easy to get covered quickly.

Amplify your financial future with cash value building policies

Some permanent life insurance may build cash value over time, subject to policy charges, crediting/investment performance, and policy terms. Some people prefer to get the minimum possible coverage for death expenses and then forget about it. There’s nothing wrong with that.

But life insurance can be more than that. Amplify can play a role in building additional vehicles for financial security through your life insurance policy. You get the peace of mind of protecting your family when you’re not around, and you also get a policy that you can leverage while you’re alive.

Learn more about how you can build tax-advantaged wealth with life insurance.

Frequently Asked Questions

How do I choose the right type of life insurance?

How do I choose the right type of life insurance?

What is whole life insurance?

What is whole life insurance?

How can I evaluate whether a life insurance platform is reputable?

How can I evaluate whether a life insurance platform is reputable?

Note

This content is for educational and informational purposes only and is not financial, investment, tax, or legal advice. It is not an offer to sell or a solicitation to buy insurance. Coverage is subject to eligibility, underwriting, and approval. Premiums, rates, features, and availability vary by state, carrier, age, health, and other factors. Policy benefits, exclusions, limitations, definitions, and terms are governed solely by the issued policy.

Amplify and Ethos are insurance distribution platforms (not the issuing insurance companies). Policies are issued and underwritten by unaffiliated life insurance carriers, which vary by product and state. This comparison is general in nature and may change over time.

Cash-value life insurance (including indexed and variable universal life) may build cash value, but cash value growth is not guaranteed and may be reduced by policy charges and expenses. Indexed universal life is not directly invested in the stock market; interest credits are based on an index-linked formula and are subject to caps, participation rates, and/or spreads, which may change. Interest credited can be 0% for a period.

Variable universal life involves investment risk, including possible loss of principal. Variable products are offered by prospectus—read it carefully before investing.

Loans or withdrawals reduce cash value and death benefit, may cause the policy to lapse, and may result in taxable income. Tax treatment depends on your situation and policy design; consult a qualified tax professional. “Living benefits” riders may not be available in all states, may cost extra, and are subject to eligibility requirements and policy terms. Customer ratings reflect individual experiences and are not a guarantee of future results.

Continue Learning

Ready to get your estimate?

A personalized plan for you.

Continue