Is Permanent Life Insurance Tax-Deductible?

Let’s rip the bandaid off: Life insurance isn’t tax-deductible, especially if you’re paying for a policy for yourself. But what is available is tax optimization through your life insurance policy. Unlike a 401K, mutual funds, or stocks, money grown as part of a permanent life insurance policy can be accessed tax-free. What does that mean for you? Big savings. B.I.G. savings when it comes time to use your cash. Let’s explore what you can do with the significant tax benefits from permanent life insurance.

Tax-advantaged Growth You Can Borrow Against

Permanent life insurance policies with cash value offer policyholders an awesome benefit: access to tax-free growth that you can benefit from if you start your policy sooner rather than later. Once you’ve built up that cash value, you can take it out and never have to pay it back or borrow against it and keep earning interest on your borrowed cash. That’s right- as long as you’re still paying for your premiums and your policy is active, you can take out your money and it can still be growing for you.

No Taxes on Your Growth

Even though the answer to “Is permanent life insurance tax deductible” is no, here’s the good news: Your premiums are paid with post-tax money, and you don’t have to pay taxes once money is already inside a life insurance policy. Compared to investing in other types of brokerages accounts, stocks, 401K, real estate, etc. where you have to pay taxes on the money you gain, with your permanent life insurance policy, you can enjoy returns without being taxed on the growth. It’s similar to a Roth IRA, except there’s no limitations on how much you can make every year. Everyone can have a permanent life insurance policy, even babies!

No Guaranteed Loss Means A Guaranteed Win.

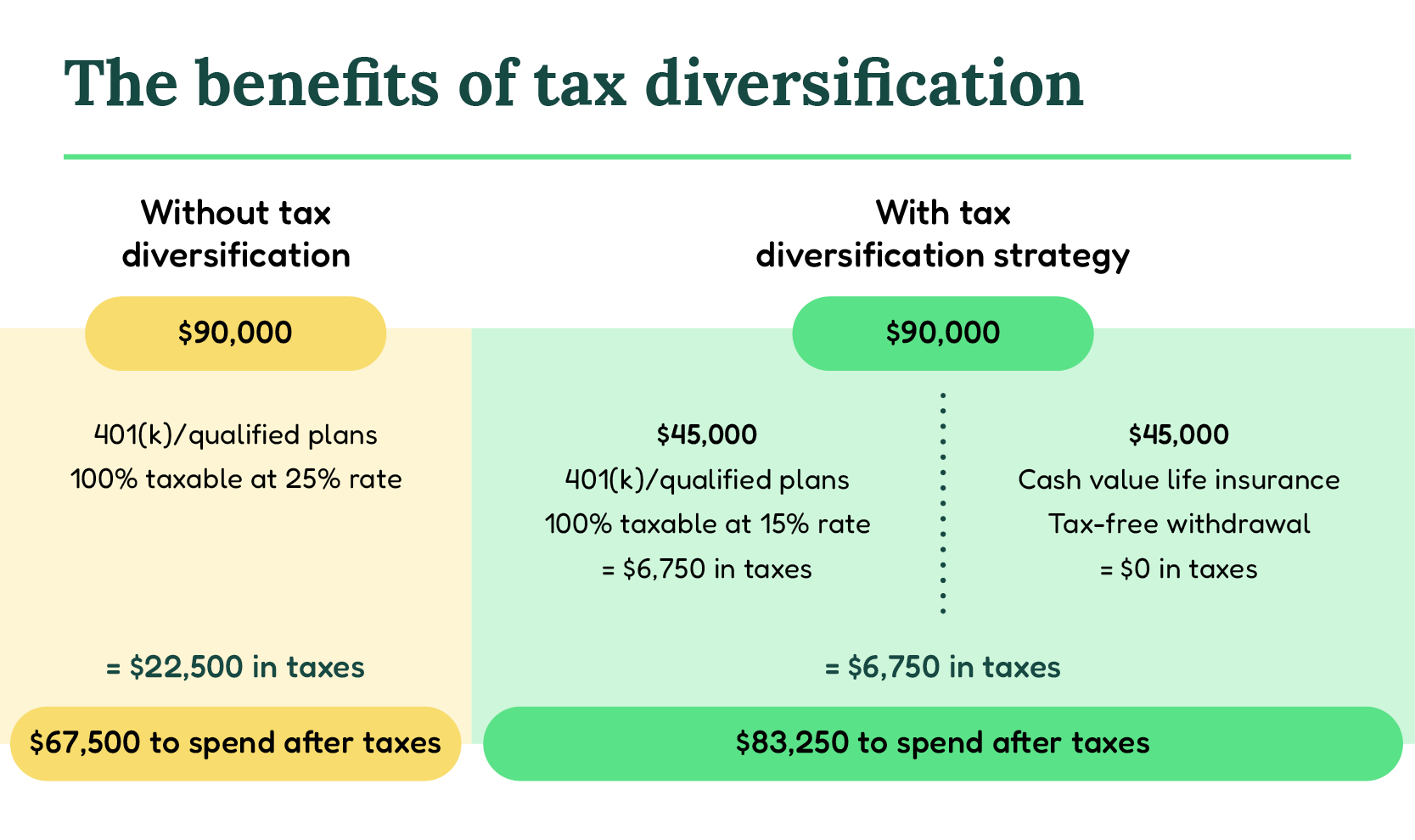

Taxes are a guaranteed loss. Money in the market has no guarantee, it might be a win, or it might be loss. But cash value in your permanent life insurance policy? A guaranteed win. With a permanent policy, you can put in 20K, 50K a year and have it grow and be accessed tax-free, which means you’re getting more, and more, and more.

You Get Dividends (If you pick a certain policy).

If you want to make investments inside of your life insurance policy, there are opportunities for dividends. And because of the tax-deferred status of permanent policies, you can reinvest them and it’s not taxed. When you break down the numbers invested and growing over time, you can actually make up to 30% more in total gains. Here’s a snapshot of the different permanent policies that we offer at Amplify and how you can use them: IUL/VUL: With a cash value component to these policies, you can build savings, get tax-free access to gains, and take out the cash value. GUL: This is the cheapest form of coverage for your entire life. This will pass down a certain amount of money to your beneficiaries or use if you get sick, but it doesn’t include a cash-value component.

There’s One Loophole (But only if you’re the owner of a C-Corp).

We saved the “what if” conversation for the end. Here goes: What if I am the owner of a C-Corp? Is permanent life insurance tax deductible then? Lucky you, the answer is yes. While we wouldn’t exactly call it kosher, if you’re an owner of a C-Corp, you can deduct the premiums from the corporate income and then bonus the difference, for both yourself and your employees. One of the ways companies do it today is by adding that bonus income directly into a permanent life insurance policy as a perk for employees. Have a question about this unique situation? Talk to our financial experts today.

TL;DR Key Takeaways

Life insurance only taxes on principle—not principal and growth like you would in other investments. Taxes are always a loss, so don’t pay more than you have to.

In life insurance, you can make 6-10% average annual returns. Since it can be accessed tax-free, you’d have to make nearly double that return in most other investment vehicles to equate to the same net gains once you factor in taxes.

We may have had to dash your dreams when it came to the question: “is permanent life insurance tax deductible?” But in reality, we gave you an even better alternative with all of the tax benefits of a permanent life insurance policy. Get started with Amplify today in just 5 minutes to start enjoying the perks for yourself.