Investing is a great way to protect your future and free up finances later in life. But what are the investment concepts you should know about before starting your journey to becoming a seasoned investor? In this guide, we’re bringing you all the details on investment concepts so you can make smarter investing decisions.

Did someone say Gordon Gekko?

Have you ever thought about investing but decided it all sounded a bit too "Gorden Gekko" and "Wolf of Wall Street" for your liking? One minute you're thinking about stocks and bonds; the next, you're beating your chest and doing some weird humming thing.

Well, don’t worry, because investing isn’t really anything like it’s portrayed in the movies–and it’s not all about stocks and bonds (though they can play their role). In reality, investing isn’t quite as exciting as a Hollywood blockbuster, but it can be very rewarding.

If you’re going to invest, you need to know about the different investment concepts and how they impact your decisions. So let’s find out a bit more about investment concepts to help you better understand the investing landscape.

Inflation

One thing you definitely want to do when investing is to protect yourself against inflation. A dollar today won't buy the same goods in 10 years' time, thanks to inflation–something you certainly want to keep an eye on.

Unfortunately, inflation isn't that easy to keep track of. It chops and changes depending on current events, rising wages, and increases in raw materials, such as oil. So you'll need to watch the consumer price index (CPI) when thinking about investing–unless you find an investment class that outperforms the growth of the CPI.

By monitoring inflation-hedged asset classes, you can help your investments thrive when inflation hits. Investments like gold and real estate income can all be resistant to inflation, but what do you do if you don’t own a ton of gold bricks or an investment property?

One way to battle against inflation is with life insurance. Investing in permanent life insurance policies can give you a cash benefit while you’re still alive, and using one to enjoy gains, dividends, and cash flow offers great protection against inflation.

Let’s say you take out an indexed universal life insurance policy. You can grow your savings at an average return of 6-8% with a cap and a 0% floor. How does that work? Part of your premiums go towards paying the cost of insurance for your “death benefit”, which will go to your family no matter how long you live, and the majority of your premiums will go to an account that grows between 0-12% annually.

This means that if the S&P 500 grows higher than 12%, you only get 12%, but if the market drops you don’t lose any money. It also means that you’re growing off of a higher amount every single year since you never suffer any losses. This way, you’re safeguarded against inflation and can enjoy potential high cash accumulation in the long term.

Growth

You don’t need to be an investment whizz to understand that growth is the name of the game when it comes to investing your money. Growth investing is an investment style and strategy focused on increasing your capital. And who doesn’t want that?

Many growth investors hit up the small or younger stocks, hoping to earn from companies whose value increases at an above-average rate compared to others in their industry. Now if that all sounds a bit too risky for you, worry not.

Permanent life insurance policies with an investment component help you grow wealth without any of the market volatility of stocks and bonds (more on that in a bit). In layman’s terms, that means you don’t pay any income or capital gains taxes on the cash-value component of your policy.

You can essentially use permanent life insurance as a wealth-building tool. Even better, you’re still paying into a death benefit, which means you leave capital to your loved ones when you pass but still prosper from the policy while you’re alive, thanks to the cash-value asset.

Taxes

If there’s one thing most of us can agree on, it’s that we all hate taxes. Important as they might be, no one ever gets excited filing a tax return unless they work for the IRS, and we always want to reduce them where possible. When it comes to investing, however, taxes are usually high up on the agenda. You make money on your investment; you pay tax on it too.

The federal government taxes investment income like dividends, interest, rent on real estate, and, you guessed it, growth and appreciation. When it comes to income taxes, the best method is to keep your taxable income low (not actual income just taxable income) and when it comes to calculating capital gains tax, it’s better to invest in tax-free vehicles like a Roth IRA, Roth 401K, or permanent life insurance policy, or hold your investment for the long term (more than one year) in brokerage account, as it will be subject to lower tax rates.

With a permanent life insurance policy you pay in for 25 years, you can withdraw the cash without paying a dime in tax. This is because the money you take out of a perm life insurance policy is 100 percent tax-free.

How does that work? Your savings is growing on top of your original coverage amount, which means both will go to your beneficiaries if you never take out your savings, and then you’re taking a loan out against that savings, which makes it tax-free.

Then, when you pass away, the amount loaned is paid off with your death benefit (which has grown over time), and the rest goes to your loved ones. That’s why it might be called a “loan”, but you never have to pay it back since you’re just taking out your own money.

Volatility

The word “volatility” sounds scary, and therefore people tend to worry about how it might impact their investment choices. Yet, volatility is one of the most misunderstood concepts in investing and actually relates to the range of price change security experiences over a given time.

If the price remains stable, then there’s low volatility in the security–and the investment remains stable too. High volatility investments can take you on a rollercoaster, hitting great highs one minute before plummeting to new lows the next.

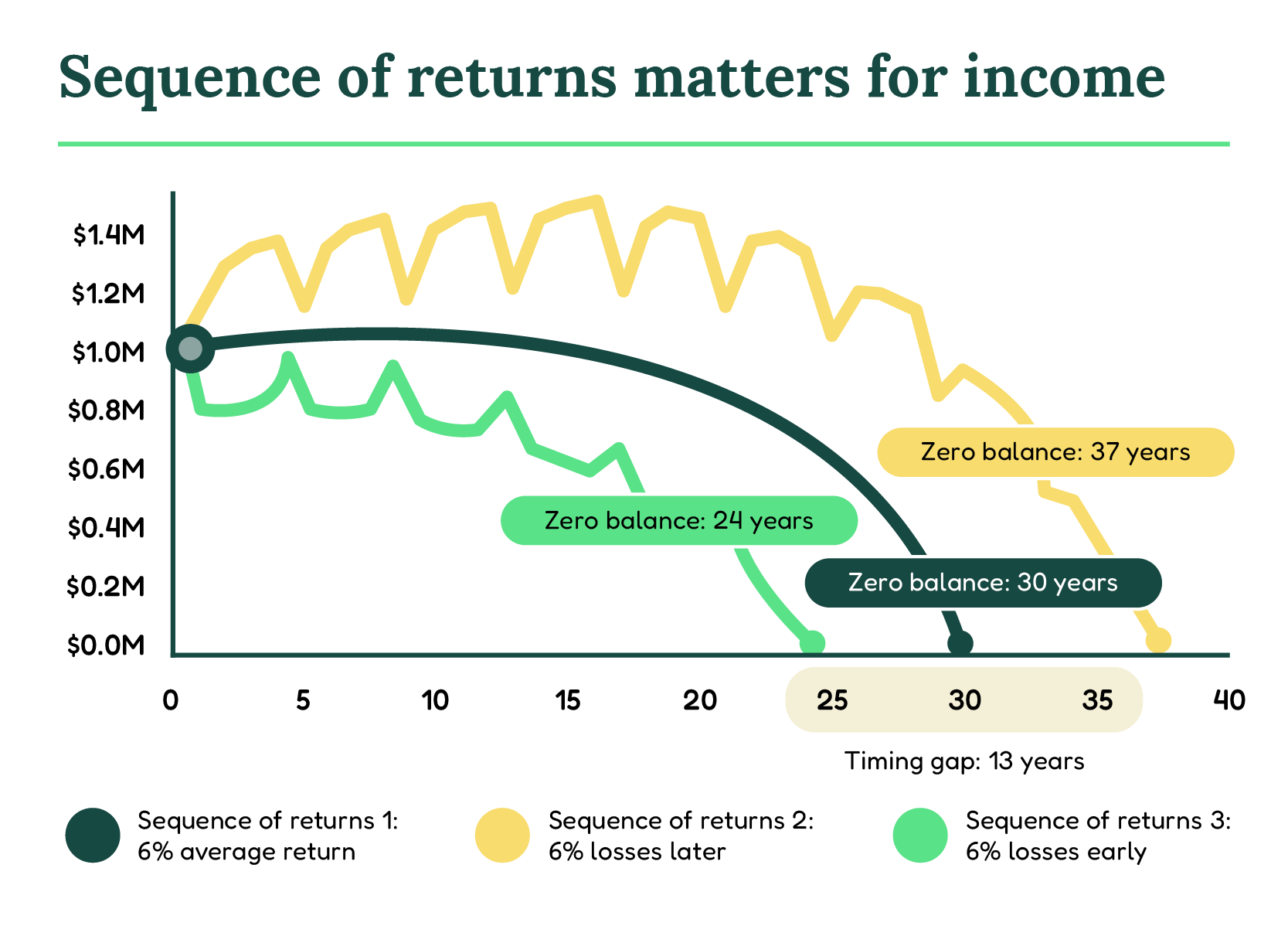

Something else to consider is the sequence of returns risk when you’re saving up for something like retirement where you’ll be withdrawing money from your nest egg periodically. Sequence of returns risk is the difference of how long your nest egg will last depending on whether the market is high or low when you start taking out money. Taking out money at a low point in the market can decrease how long your savings lasts by 10-15 years!

If you’ve got the stomach and nous for risky investments, the reward can be a quick payoff (or a crushing disappointment). But if you’re like us and prefer something a bit more stable, then you’ll want a relatively low volatility investment, like permanent life insurance.

The cash value aspect of permanent life insurance grows over time between a floor and a cap. Therefore, the benefit is never losing money but still being able to access relatively high returns, often averaging 6-8% tax-free (which is equivalent to 8-10% in a taxable vehicle like a brokerage account or 401K. It's the primary reason why this type of life insurance is referred to as a savings vehicle, and it can lower the overall volatility of your investment portfolio.

In conclusion: understanding investment concepts

Now that you have a better idea of investment concepts and how permanent life insurance can safeguard against inflation while helping accumulate growth, you can make savvy decisions about your investments. And it could all start with a permanent life insurance policy that’s just right for you.

Find life insurance that acts as an investment vehicle and looks after your future.