Most of us are happy to shell out almost $15 a month for Netflix and Apple subscriptions. And why wouldn’t we be? After all, there’s a tangible benefit (if we’re calling binge-watching Tiger King tangible). But paying a certain amount per month for something like life insurance? No, thank you. Why would I pay for something that I can’t receive until I die?

So, yeah, life insurance isn’t the quick sell that Netflix or other pay monthly services are. It’s understandable you might think that way, but it’s also misguided. That’s because life insurance is so much more than a death payment, and its monthly cost probably isn’t anywhere near as much as you think, even if it’s worth a million dollars.

But how much does a million-dollar life insurance policy really cost (or any life insurance, for that matter), and why is it worth your consideration? That’s what we’re here to tell you with our handy guide to the cost of life insurance, what it entails, and how you can use it while you’re still alive.

What are the different types of life insurance?

Before we get into the nitty-gritty of life insurance costs, you probably have a few questions about how it works. You’re also likely asking yourself why we’re so darn excited about something that’s commonly associated with death.

Life insurance isn’t just about making a payment to your loved ones after you pass away. Yes, that is a part of it. But there’s more to life insurance, with some options allowing you to benefit while you’re still alive and kicking.

There are two primary types of life insurance: Term life insurance and permanent. How they work has a major impact on how – and when – you can access them.

Here’s what you need to know about term and permanent life insurance:

Term life insurance

A term life insurance policy covers you with life insurance for a specific number of years, usually anywhere between five and 20. It’s there to give you peace of mind, just in case the unexpected happens during the time you’re covered. Term life insurance is ideal for anyone who has a temporary need for life insurance or a limited budget, as it’s the cheapest type of life insurance available and usually has a fixed rate. Once your term ends, however, you will no longer be covered and therefore will need to purchase more insurance.

Permanent policy

A permanent policy is where things get interesting. The name likely gives it away, but permanent life insurance provides you with life-long protection. You also don’t need to die before it pays out. That last sentence probably has you sitting up and paying attention, so we’ll say it again: a permanent policy gives you an option to accumulate tax-free growth with your cash value that can be accessed later in life. With a permanent life insurance policy, you can build cash value and access tax-free wealth at a later date. So you could essentially use it in retirement, for emergencies, or just because–sometimes it’s good to treat yourself, right?

Fancy knowing more about term and permanent? Here's a little something we wrote in more depth.

Can I use my life insurance while I’m alive?

Again, yes, you absolutely can. As stated above, having permanent life insurance cover means you don't need to wait until you die before you and your loved ones benefit. That's because of things like tax-free initiatives and the ability to build the cash value, which can be used when you retire.

That sounds great, but how much does life insurance cost?

See, we told you life insurance needn't be a morbid subject. You’re probably even looking at your Netflix subscription and wondering if you should cancel it to focus on your future. Fortunately, you can probably have both. That’s because life insurance can be as little as $50 per month for $100,000 or more that you or your family is guaranteed to receive. That’s about the same as a dinner out with drinks!

That being said, how much you pay depends on several different factors. Things like gender, tobacco use, family medical history, past medical history, and current health are just some of the factors considered when taking out a policy.

Your age also plays a vital role, and the younger you are the cheaper your cover is. So it's definitely something you should give serious consideration to if you're in your 20s, 30s, and 40s. Life insurance isn't just for those reaching the later stages of their lives.

Other aspects include the type of cover you get, with permanent life insurance typically costing more (for the reasons stated above) than term life insurance, which is a cheaper, fixed monthly rate.

What about the big bucks? How much does a million-dollar life insurance policy cost?

If you're thinking about getting a million-dollar policy, you must be feeling all the vibes about life insurance. And we're here for it. The good news is that it's not that expensive, with a million-dollar life insurance policy costing around $50 per month on average. You can even get a certain amount of that million in permanent coverage, which you can take out for retirement or use for health emergencies.

Of course, there are many factors to consider, and everyone's personal circumstances are different. But it's good to get a ball-park figure. So, now you know how much it might cost, how about understanding why a million-dollar life insurance policy could be beneficial?

Why do I need to take out a million-dollar policy?

To address the elephant in the room, no, you don’t need to be a millionaire to get life insurance cover worth a million dollars. If you are one, that’s great; keep at it. But if you’re like most of us, being a millionaire is still on the “to-do” list.

When it comes to life insurance, however, it's a different story. Million-dollar life insurance policies are quite common, and having one can give you even more peace of mind as you build your future.

If you’re in a scenario where you and your partner are both earning around $50k per year and have children and a mortgage worth $300,000, a one million dollar life insurance policy could make sense.

Should the worst happen, it’s recommended that you should get enough coverage to replace your income for 10 years and take care of the mortgage so that your family can be financially stable during that time. A million-dollar policy can help cover the costs to maintain their lifestyle while potentially paying for things like college tuition and living expenses.

How do I know if I qualify for a million-dollar policy?

Whether or not you qualify comes down to factors like age, income, health, lifestyle, and length of coverage. You can always get a quote to see if you qualify and know the exact amount you will pay each month.

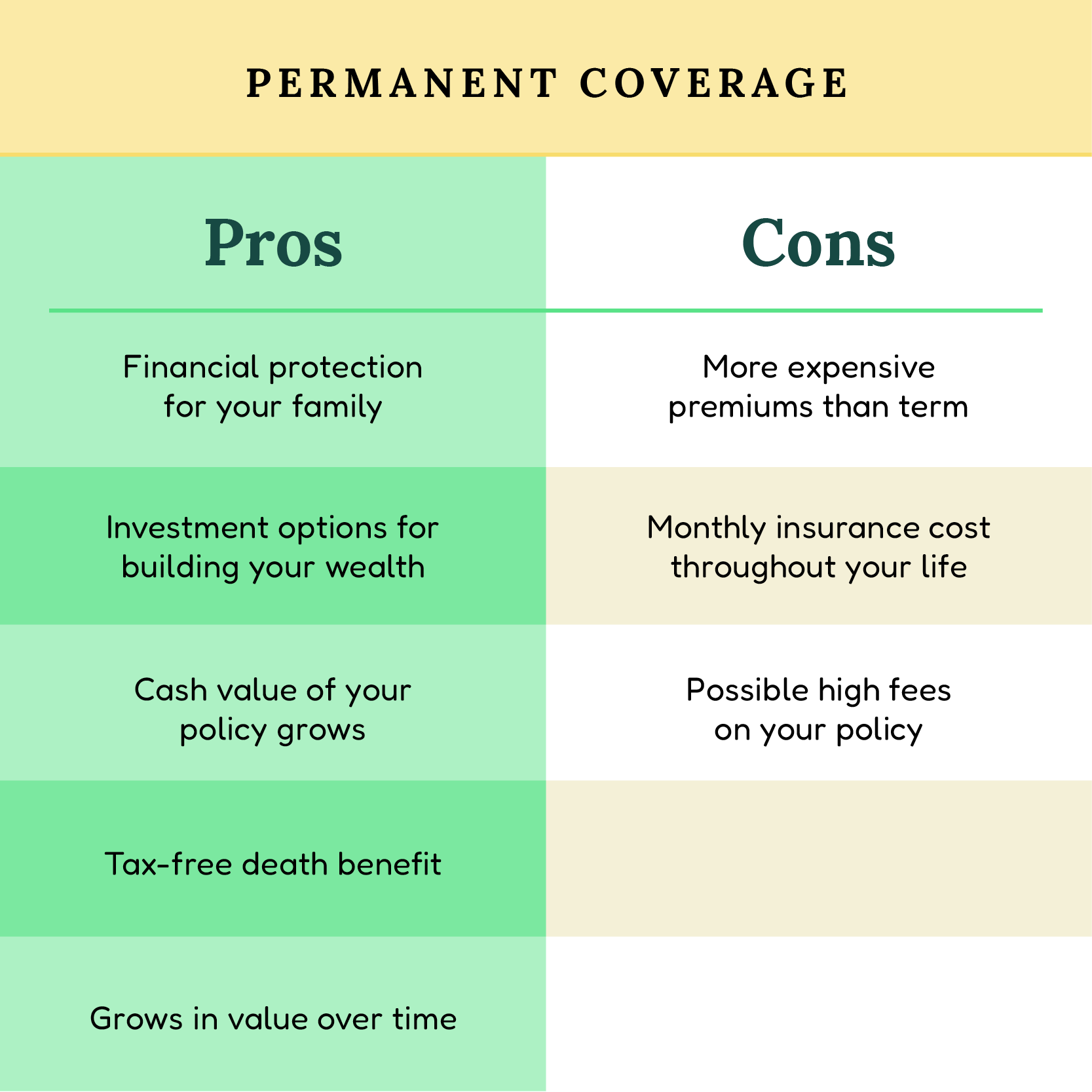

What are the pros and cons of life insurance?

We’re almost at the end of this guide, and it’s been a lot. But before we sign off, let’s round it up with the pros and cons of getting life insurance, specifically focusing on permanent coverage. Now, you might choose cover worth a million dollars; you might not. Either way, it’s good to have the facts, so here they are:

In conclusion: Having a clearer understanding of how much life insurance works and what it costs

Life insurance really doesn't need to be a conversation about the big D-word. Instead, it can help you protect your future while growing your wealth. And with policies like permanent insurance, you can reap the rewards while you're still alive. That means even more Netflix binge-watching while safeguarding your financial future. Amplify can help get you there.