Most parents aren't lying awake thinking about life insurance for their kids. They're thinking about school supplies, soccer practice, and how to stretch the grocery budget a little further.

But a growing number of families are considering how to support their children's long-term financial well-being while addressing immediate day-to-day needs. One option that may help, depending on your family's goals and budget, is a well-structured whole life insurance policy for your child.

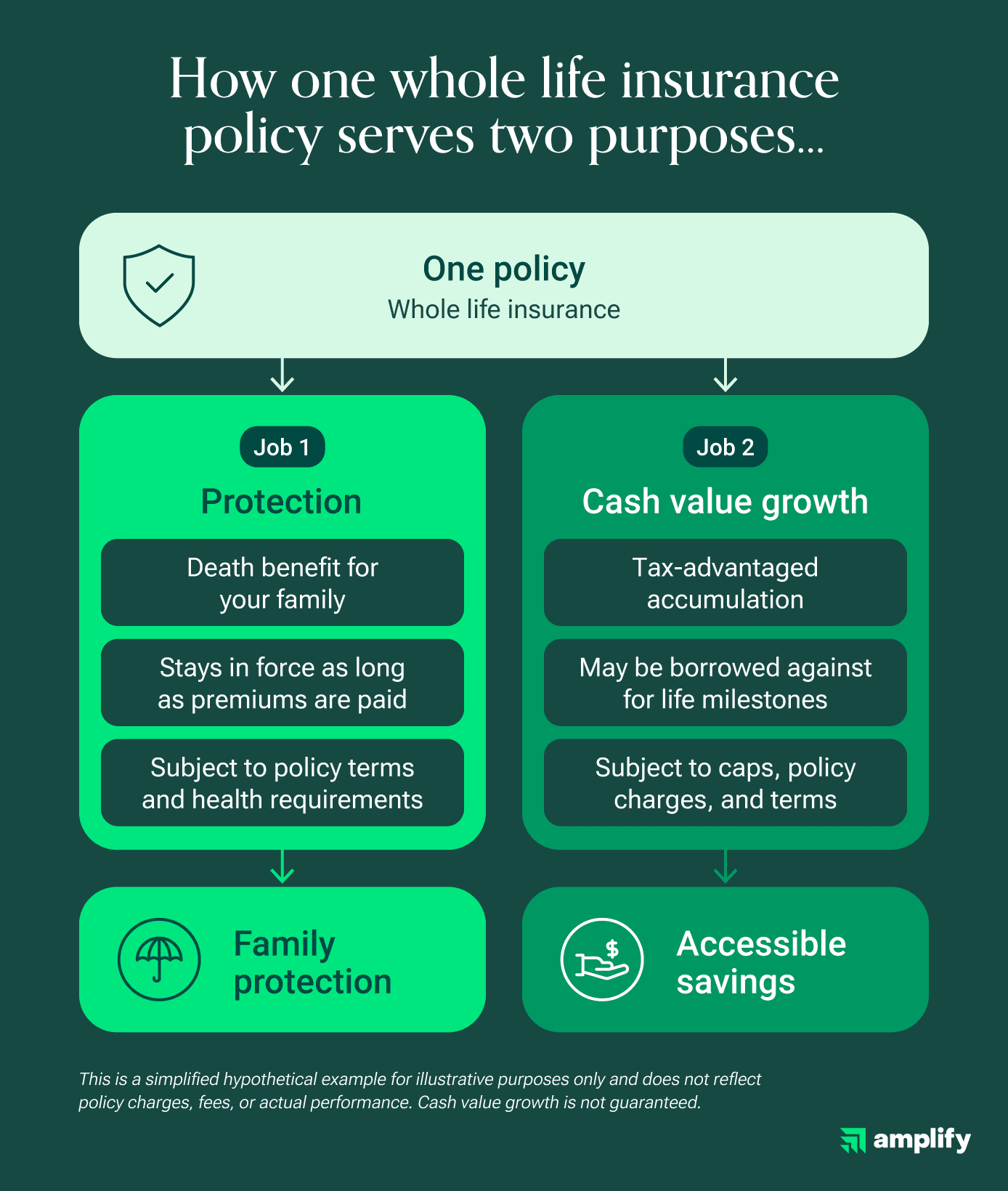

The best whole life insurance policy for a child can be part of a long-term financial strategy that combines death benefit protection with potential cash value accumulation, subject to policy terms, costs, and continued premium payments.

A well-structured policy can provide a mix of death benefit protection and potential tax-advantaged cash value growth over time, subject to policy terms, costs, policy charges, and continued premium payments.

This guide breaks down whole life insurance options for children, explains how these policies work, and helps you decide whether this strategy makes sense for your family.

Most people haven't heard of this approach before, and that's exactly why we're here.

Whole life insurance options for a child

Strong whole life insurance options have a few things in common. They may include features such as potential cash value growth, clear fee information, and dividend potential, though cash value growth and dividends are not guaranteed.

For this overview, we considered factors families often compare when reviewing whole life insurance options for children, including financial strength information, potential cash value accumulation, underwriting requirements, available riders such as guaranteed insurability, and digital accessibility.

Here's how selected carriers and platforms compare.

Methodology: This overview is informational and not a ranking or recommendation. Options were selected based on publicly available information about market presence, independent ratings, consumer reviews, and relevance to families prioritizing both death benefit protection and potential long-term cash value accumulation. Pricing estimates are approximate and vary by age, health, coverage amount, and policy terms. Always request a personalized premium estimate before making a decision.

1. Amplify

Best for: Potential cash value growth and digital experience

Amplify is a modern, digital-first platform designed for families who want clear insight into their life insurance. Amplify uses technology to help parents visualize a policy's potential growth over time, subject to policy terms, charges, and performance.

Amplify's technology-driven approach is designed to make it easier to visualize how a policy may grow over time, subject to policy terms, charges, and performance.

Amplify CEO Hanna Wu describes the platform's mission simply: "You're working hard every day, and at the end of the day, you know that you're putting your family in a better place."

Policies may offer tax-advantaged cash value accumulation, subject to policy terms, costs, charges, and performance. Visual tools help parents track potential growth alongside their family's other financial goals, but projected values are not guaranteed.

Key features:

- Digital-first application: Apply and manage your policy online, with licensed support available when needed

- Clear disclosures: See fees, charges, caps, and how cash value may accumulate

- Tax-advantaged cash value: Understand how policies may build cash value that could be accessed for life milestones, subject to policy terms and costs

- Visual planning tools: See projected policy growth over time

- Agent Assist: Speak to a licensed professional at any point in the process; they'll have full context on your application

Coverage: Varies by policy; subject to eligibility and policy terms

Pricing: Varies by age, health, and coverage amount

2. Mutual of Omaha

Best for: Simple, small-benefit coverage

Mutual of Omaha has one of the most recognized names in insurance for a reason: its Children's Whole Life product is simple, affordable, and straightforward.

For parents focused primarily on the death benefit, Mutual of Omaha is worth considering. Their children's policies typically offer $5,000 to $50,000 in coverage, often with simplified underwriting that doesn't require a medical exam for standard amounts, though issuance may depend on health questions and policy terms.

A key feature is the guaranteed purchase option, which may allow your child to purchase additional coverage later in life without additional evidence of insurability, subject to policy terms.

Key features:

- Simplified underwriting: Often, no medical exam is required for standard coverage amounts, though issuance may depend on health questions.

- Guaranteed purchase option: May enable your child to increase their coverage in the future without undergoing further medical qualification, subject to policy terms.

- Streamlined approval: Standard coverage levels frequently do not require a medical examination, though issuance may depend on health questions.

- Future coverage options: May offer the opportunity to obtain extra insurance later in life without a health review, subject to policy terms.

- Level premiums: Premiums are designed to remain unchanged throughout the life of the policy, subject to policy terms.

Coverage limits: Available from $5,000 to $50,000.

Cost structure: Budget-friendly monthly rates that fluctuate based on the child's age when the policy starts and the chosen benefit amount.

3. Gerber Life Insurance

Best for: Brand recognition and potential automatic increases

Gerber Life's Grow-Up Plan is one of the most recognized children's life insurance products in the U.S., and it has a feature that may appeal to parents: when the child turns 18, coverage may double while the premium stays the same, subject to policy terms.

That means a $25,000 policy may become a $50,000 policy at the same premium. No medical exam may be required for standard coverage amounts, though issuance may depend on health questions and policy terms.

Key features:

- Potential coverage doubling: Coverage may double at age 18 at the same premium, subject to policy terms.

- Simplified application: No medical exam may be required for standard coverage amounts, though issuance may depend on health questions.

- Transferable policy: The child may take over as owner at adulthood, subject to state law and policy terms.

Coverage: $5,000–$50,000; coverage may double at age 18, subject to policy terms

Pricing: Starting around $3.70/month; varies by age and coverage amount

4. MassMutual

Best for: Dividend potential

MassMutual is a mutual company, which means policyholders may be eligible to receive dividends, though dividends are not guaranteed and depend on company performance. When received, dividends may help increase the policy's cash value or death benefit over time, subject to policy terms and charges.

Their policies tend to start at $50,000+ and offer a variety of riders that may support long-term care, estate planning, and other needs, subject to policy terms. An insurance professional can guide the setup process.

Key features:

- Dividend eligibility: Policyholders may receive dividends based on company performance (not guaranteed).

- Available riders: Options that may help match the policy to long-term care, estate planning, and other needs, subject to policy terms.

- Insurance professional-guided setup: A licensed professional can help review policy options in light of your family's goals.

Coverage: $50,000 and above; varies by policy design

Pricing: Higher premiums relative to simpler products; varies by age, health, and coverage

5. Northwestern Mutual

Best for: Long-term financial planning

Northwestern Mutual has publicly reported financial strength ratings from rating agencies such as A.M. Best and Moody's, which may be relevant when you're buying a policy designed to last decades.

Their insurance professionals may help families consider how a child's policy fits with estate planning, retirement diversification, or long-term financial goals.

Coverage amounts and premiums vary significantly by policy design and require an advisor consultation.

Key features:

- Insurance professional-guided setup: Reviewed in the context of a broader family financial plan.

- Estate and legacy focus: Designed for families considering multigenerational planning.

- Cash value access: May be borrowed against for major life milestones, subject to policy terms and accumulated value. Policy loans accrue interest and may reduce policy values and death benefits.

Coverage: Varies by policy design; advisor consultation required

Pricing: Varies; requires a personalized quote through a Northwestern Mutual advisor

What is whole life insurance for children, and how does it work?

Whole life insurance for a child is a type of permanent life insurance purchased by a parent or grandparent for a minor. Where term insurance covers a set period and expires, whole life insurance is designed to last a lifetime, as long as required premiums are paid and policy terms are met.

When you pay your monthly premium (what you pay in), a portion covers the death benefit, which is the money your family would receive if something happened to the child. Another portion may build cash value over time.

That cash value may grow tax-advantaged, subject to policy terms and costs, and it has more uses than most people realize. As the policy builds value, it may be possible to borrow against it for tuition, a first home, or other milestones. Loans accrue interest, and outstanding balances may reduce the death benefit or affect tax treatment if the policy lapses.

The difference between whole life insurance for a child vs. whole life insurance for adults

Both products are permanent life insurance, but they serve different purposes and work differently in practice. Parents or grandparents typically own the policy while the child is a minor.

At the age of majority (usually 18 or 21, depending on state and policy terms), ownership can transfer to the child.

At that point, coverage is already established, and cash value may have been accumulating for years. This head start is worth considering when deciding whether permanent coverage makes sense for your child.

Here's a side-by-side look:

Pros and cons of starting life insurance coverage early

A child's whole life policy should be considered as part of a broader strategy. The right fit depends on your family's goals, budget, and priorities.

Here's a straightforward breakdown of the trade-offs. For a fuller picture of how this fits into family life insurance plans, the context matters.

Factors that influence the cost of a child's life insurance policy

Several factors shape what you'll pay for a child's whole life policy. Coverage decisions may look different depending on your household structure, too: single parents often weigh these choices differently than dual-income households.

- Age at enrollment: Life insurance for babies may be available as early as 14 days old at some carriers; younger applicants typically pay lower premiums, and coverage may be easier to obtain earlier in life, subject to health questions and policy terms

- Coverage amount: A larger death benefit means higher premiums; most parents start with $25,000–$50,000

- Health at time of application: Many carriers offer simplified underwriting for children, though health questions and significant health conditions may affect approval, pricing, or available coverage

- Payment frequency: Some carriers offer a small discount for paying annually rather than monthly

- Riders: Adding a guaranteed insurability rider may increase cost, subject to policy terms

- Policy design and carrier: Fees and structure vary by company

Pro tip: Look beyond the premium. Ask about the cash value accumulation schedule, built-in fees, and how the guaranteed insurability rider works.

How to choose the right policy for your family: 9 tips

Choosing the best life insurance policy for a child comes down to matching the right product to your family's goals, budget, and ability to keep required premiums current. Here's a practical checklist:

- Define your primary goal: Protection (death benefit), long-term savings (cash value), or both? Your answer shapes which product type makes sense

- Set a realistic budget: Choose a premium you can consistently maintain. Lapsed policies may have tax and financial consequences

- Check financial strength ratings: Look for carriers rated A or higher by A.M. Best

- Compare at least three providers: Use the table above as a starting point, then request personalized premium estimates

- Read the fine print on cash value access: Know when and how cash value may be accessed, any charges involved, and what happens if you take a loan

- Address your own coverage first: If you don't yet have sufficient coverage yourself, that's the priority

- Ask about riders: A guaranteed insurability rider may allow your child to buy more coverage later without a medical exam, subject to policy terms

- Name your beneficiary thoughtfully: How you name a child as beneficiary involves key decisions worth understanding before you finalize the policy

- Consider the full picture: A qualified professional can help you weigh this alongside education savings, a Roth IRA, or other financial options, recognizing that life insurance serves a different primary purpose than those products

Whole life coverage for their whole life

Whole life insurance for a child may play a role in a family's long-term financial plan, whether the goal is death benefit protection, potential tax-advantaged cash value accumulation, or both, subject to policy terms, costs, charges, and continued premium payments.

Whole life insurance through Amplify is built for families who want death benefit protection and the potential to build cash value over time, subject to policy terms, costs, charges, and performance.

Explore coverage options, get a personalized premium estimate, and receive guidance online, or speak to a licensed professional at any point in the process.