Choosing a life insurance policy means picking between term and permanent life options. And if you opt for the latter, there are even more decisions to make, like which type of permanent life insurance is right for you. For many, the answer is variable universal life (ULI) insurance. But just what is VUL, and how can it help you? We've got the answers below in this guide to variable universal life insurance.

What is variable universal life insurance?

Variable universal life (VUL) insurance is another type of permanent life insurance. Just like a perm policy, it comes with fixed premiums, a death benefit, and cash value, which allows you to accrue money over time and tap into it while you're still alive.

It's also designed for the long term, with a VUL policy staying intact throughout your life–or as long as you make the payments on the premiums. Consequently, you get long-term stability and the opportunity to grow the cash value and death benefit over time.

There are some key differences from a perm policy, however. These include having investment flexibility with the cash value as well as how the premiums are paid and the level of the death benefit.

You decide on the amount and frequency of premium payments (with limits involved) and have the option of making lump-sum payments or using the cash value towards the premiums (more on that later).

Essentially, a VUL is a separate account with funds tied to the market and a fixed account. In that sense, it's similar to variable life as you can invest in underlying sub-accounts offering a variety of investment options, including stocks, bonds, mutual funds, and money market securities.

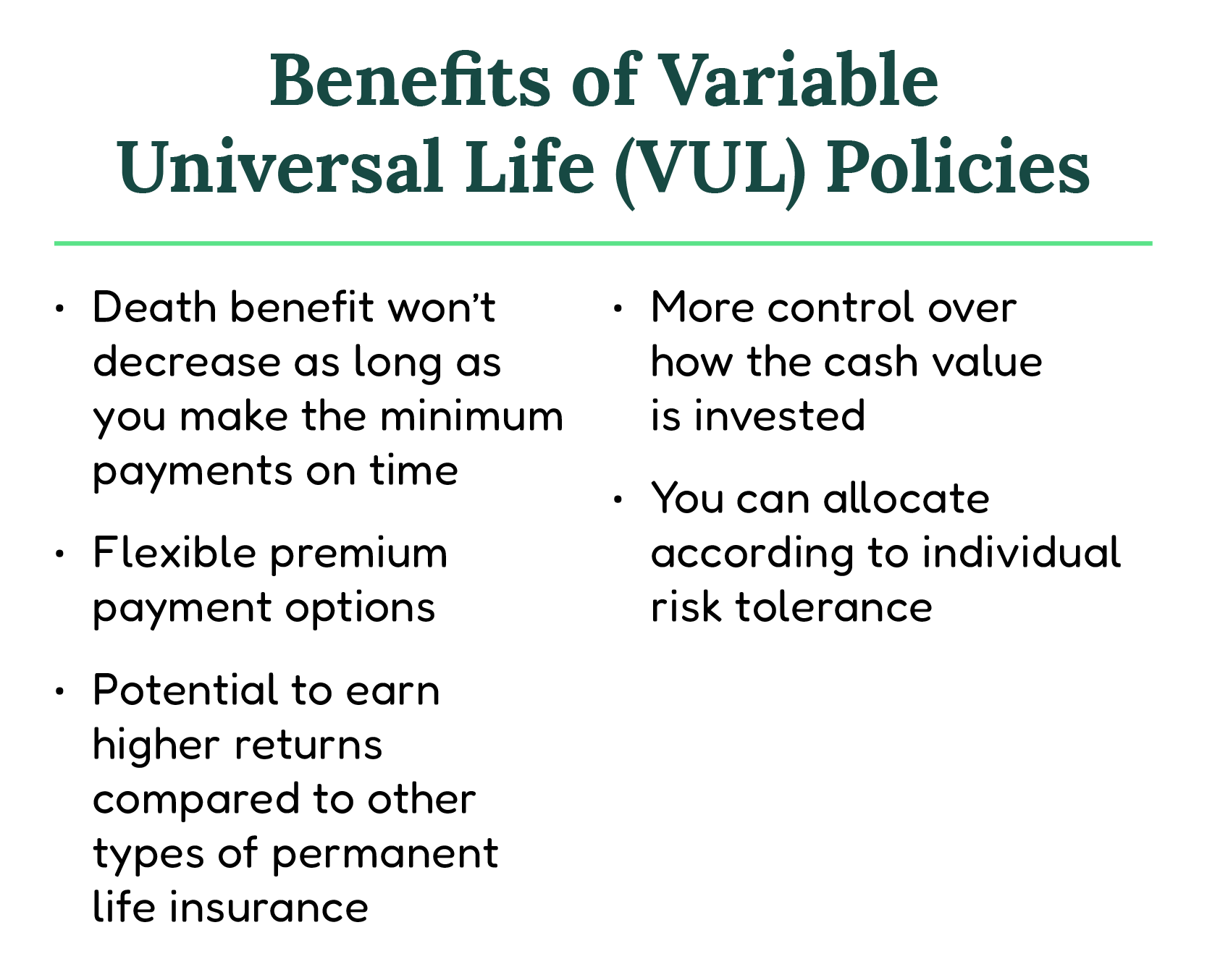

Key features and benefits

Adjustable premiums

With a VUL, you get adjustable premiums and the ability to skip a payment or even stop paying your premiums if the cash value has enough in the pot to cover them. This feature was taken from universal life insurance and added to the variable element to give policyholders more choice and flexibility over their coverage.

Investment variety

You can potentially earn more with a variable universal life insurance policy as it lets you invest in underlying sub-accounts with a breadth of investment options. The investments are tied to financial markets, meaning the value of your policy fluctuates as the investment goes up or down. The reward is higher than other forms of life insurance, but so too is the risk, and your cash value could depreciate in a poor-performing market. It's also possible to lose the death benefit if the policy lapses by policy provisions. There's also the benefit of transferring funds between investments tax-free, meaning there are no tax implications involved.

A VUL policy lets you choose from a number of investment options, such as stocks, bonds, or even a combination of the two. There’s also the option of investing in a fixed account, and doing so provides a guaranteed minimum interest. When the investment is up, your policy is worth more, and when it’s down, so too is your policy.

Increase the death benefit

One of the key benefits of a variable universal life insurance policy lies in its flexibility. If your insurance needs change over time, you can adapt the policy, opting to increase or decrease coverage as you see fit. You can increase the death benefit or make a lump-sum payment to boost the policy's cash value.

Withdraw or borrow from it

Much like other forms of permanent life insurance, you can withdraw the funds or take a loan against the cash value with your VUL coverage. Doing so may reduce your death benefit, but if you have a solid number saved against it, you can still decrease the death benefit and have enough to leave your beneficiaries after you pass away.

How does VUL differ from universal life insurance?

Universal life and VUL are similar in many aspects but for a few nuances. VULs offer more investment options, and you can select a number of different funds to create a portfolio of investments. Regular universal policies don’t have this option, though you can select a policy with features designed to suit your needs. For example, there’s an option to go for a fixed interest rate or one that fluctuates with the stock market.

Who is a good candidate for VUL?

Variable universal insurance is popular with people looking for maximum flexibility with their life insurance policy. It’s highly customizable and allows you to adapt the coverage to your current circumstances, whether that’s changing the death benefit or using the cash value to cover the premiums.

Suppose you view life insurance as a form of protection and an investment opportunity. In that case, you might look favorably on variable universal investment accounts–especially if you understand how things like stocks and bonds work.

You can take a hands-on approach and monitor investment performance, making decisions about where to allocate funds and how to make the most out of the investment. Just remember: investing involves risks that have the potential to lower the policy’s cash value.

And who isn’t?

If you're someone who doesn’t like taking risks, then a VUL might not be for you. Many people opt for a more traditional form of permanent life insurance, which comes with increased stability over a VUL policy and doesn’t require you to monitor aspects like the stock market.

In conclusion: Getting variable with VUL

As long as you’re aware of the risks involved and understand that the cash value could depreciate with a poor-performing market, a VUL can be a handy option for anyone who wants more control over their policy. Getting a variable universal life insurance policy can be a smart move if you want more flexibility and control over the cash value accumulation. With the right investments, you can grow its value more than you can with other forms of life insurance–and that’s an appealing reason for many to get variable universal life insurance.

Use our handy VUL calculator and see an estimate of how much money you can grow.